|

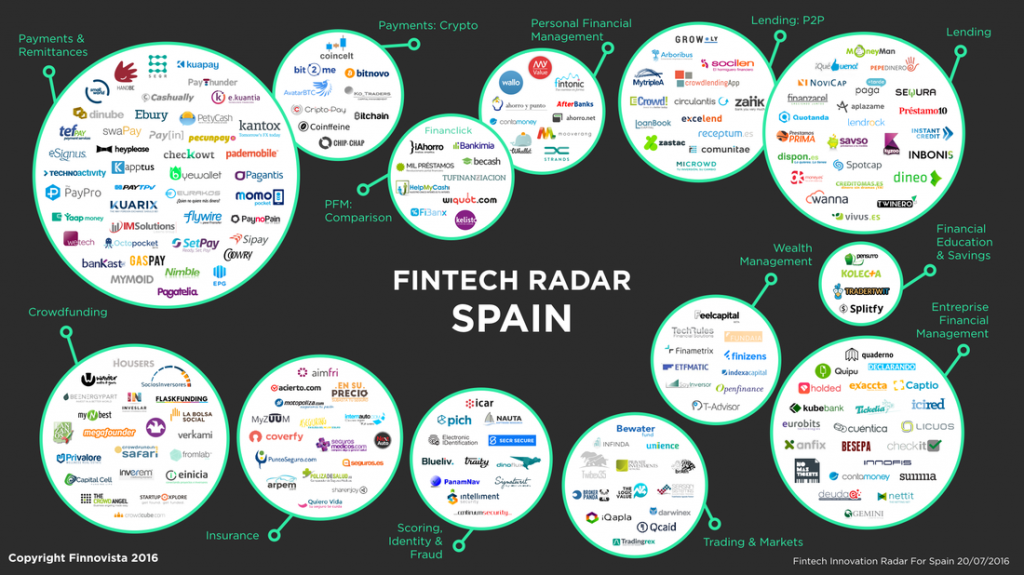

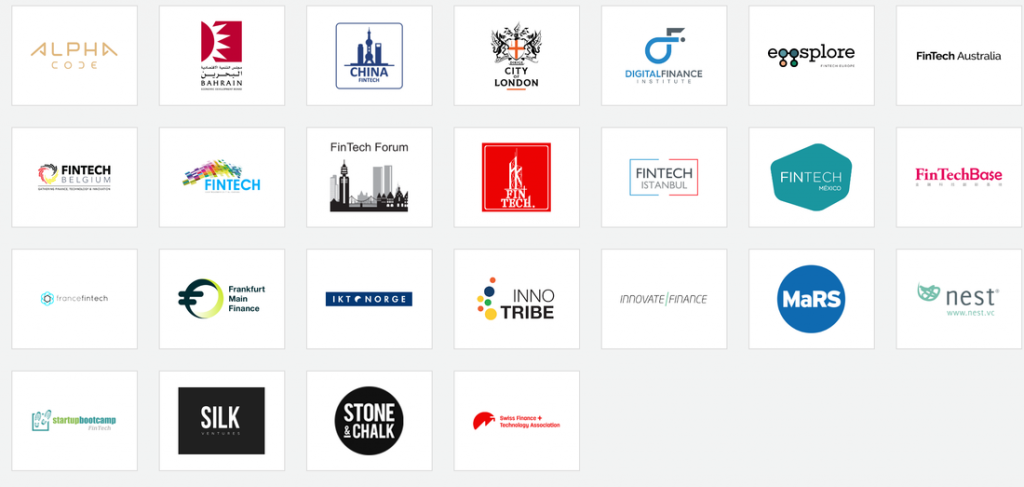

Fintech has not been on the radar in Spain long, it was long not known by most of the people and with just 50 financial technology companies, and with few successes. But things have improved quite rapidly and accordingly to Fintech Radar Spain 2016, prepared by Finnovista, the sector can now count 208 startups, with a 400% increase in just three years, and few players that are making waves. The fintech industry has growth at an impressive rate, not just in Spain but also in other parts of the world, presenting an opportunity for the country to modernize the financial sector and the banking system. What’s interesting about Spain in particular is that it has seen a growth in the whole technology sector, despite the economic crisis that has gripped harder than in most of other countries, and the confused political situation. But it’s not only the recent successes and the abundance of talent that makes Spain well positioned with Fintech, it’s also about the role that it can play with the LATAM countries, on which its connections are always strong. With 208 startups, Spain is now the largest fintech market in Ibero-America, followed by Brazil with 130, Mexico 128, Colombia 77 and Chile with 56 financial technology ventures. With 80% of fintech startups offering products and services for consumers (B2C), this presents a clear threat or opportunity for those ready to take it, for Spanish banks. Some banks are leading the way, for example BBVA that has created a $250 million fintech fund, and bought two financial technology companies in the last year - Simple, an American online-only bank, for $117 million, and Holvi, another digital bank this time from Finland, for an undisclosed amount - it seems clear that most traditional financial players still have to realize the big opportunity they now have with this new wave of innovation. More cooperation, partnerships, and acquisitions are in sight, not only in Spain but also elsewhere, as banks, insurance companies and more in general all the traditional financial players, are on a steep learning curve. Think for example about the 600 bank branches that have been closed down in Spain in 2015 alone, that the sector has no alternative but to embrace technology and innovation for more growth. Read the whole article on Crowd Valley News.  In a post published on our blog last year, we described Islamic Finance as 'one of the next frontiers of crowdfunding', saying that we could certainly expect to see more and more ‘digital investing conducted under Islamic Finance principles’. Striking as it is, the utilization of financial technologies to enable the growth of a millennial sector shouldn’t come as a surprise: looking at the history of Islamic Finance, the sector has always benefited from financial innovations - sometimes even pioneering them. The Suftajah for instance was an answer to the need to secure the integrity of money transactions. This form of bill of exchange or letter of credit later became the foundation on which many other financial instruments in use today were developed. According to the IMF, Islamic finance assets grew from $200 billion in 2003 to $1.8 trillion at the end of 2013, making it one of the fastest-growing sector within the financial industry. And yet, Islamic Finance still represents less than 1% of the global financial industry, which leads analysts to predict this market to reach a stunning $3.4 trillion by the end of 2018. Today, 5 countries (Malaysia, Saudi Arabia, the UAE, Kuwait, and Qatar) hold more than 60% of the global Islamic Finance assets with a clear gap between the top two (Malaysia and Saudi Arabia) and the rest. Indeed, both countries respectively own more than 20% of all Islamic Finance assets. The vast majority of those assets can be found in Islamic Banks (this segment representing more than 75% of global assets), but other fast-growing segments are of significant importance. The Sukuk market for instance: representing 18% of global assets, Sukuk is a product similar to asset-backed securities, except that it doesn’t pay interests and its performance is entirely linked to the one its underlying assets. In that spirit, the first Islamic banking internet-based platform that combines the expertise of Islamic banks and the efficiency of technology was created in Malaysia. The Investment Account Platform is backed by six Malaysian Islamic banks, and its purpose is to become a central marketplace to finance SMEs whose activities fall within the Islamic law. In the words of Muhammad bin Ibrahim, governor of the Central Bank of Malaysia, this initiative “opens up new possibilities for improving efficiencies, reducing wastage and enhancing the customer experience”. Ultimately, it will provide “opportunities for industry players to radically transform operational models by adopting digitization strategies that will be able to deliver much greater scale”. At Crowd Valley, we look forward to partnering with both established institutions and new innovators to provide more services and value to the end users as the financial services market continues its modernization in the Islamic Finance sector. Read the whole article on Crowd Valley News. China announced rules to tighten regulation of the national $60 billion P2P lending industry, with a document issued by the Ministry of Public Security, China Banking Regulatory Commission (CBRC), the Ministry of Industry and Information Technology, and the Cyberspace Administration of China. The new regulations took effect on August 24, 2016, but platforms now have one year to adapt their practices according to the framework. This is the first comprehensive framework for regulating P2P lending in China, an industry that has seen a huge growth in the past few years, along with some issues with risk management and fraud. According to Bloomberg there were a total of 982 billion yuan ($147 bn) of loans in 2015, with a 400% increase on the year before and approximately 10 times more than in 2013. The market attracted over 3.4 million investors and 1.15 million borrowers in July 2016. With the new rules a single person can borrow a maximum of 200,000 yuan ($30,000) from a platform and a total of 1 million yuan ($150,000) in aggregate from different P2P platforms). For corporations the caps are five times higher, with the opportunity to borrow 1 million yuan ($150,000) on a single platform and 5 million yuan ($750,000) in aggregate. Read more on Crowd Valley News!  There has been no shortage this presidential election of talk of the effects of international trade agreements, and specifically the Trans-Pacific Partnership (TPP). The TPP has long been a priority of President Obama and is currently awaiting ratification. Congress granted the President "fast-track" authority, meaning lawmakers can only reject or ratify the finished product without any additions or amendments. But what is exactly is the TPP? The TPP is regional trade agreement with the aim of lowering tariffs and fostering trade among the 12 member nations, including: The US, Mexico, Canada, Peru, Chile, New Zealand, Brunei, Sinapore, Malaysia and Vietnam. Around 18,000 tariffs will be affected in some way after ratification. This includes a large perecentage of manufactured goods and almost all US farm products. It is still largely up in the air whether or not the TPP will be ratified under President Obama or if lawmakers on both sides of the aisle will elect to wait until after the November election. Read more on TradeUp Blog.  The Global Fintech Hubs Federation (GFHF), has been announced on August 25, 2016, on initiative of Innotribe and Innovate Finance, to foster innovation across the world’s financial services industry and help startups and institutions gain visibility into new markets. Stakeholders from more than 20 cities around the world, including London, Shanghai, Frankfurt, Istanbul and Nairobi, have already decided to join the federation, with more groups to come. The declared mission of this new federation, that will be formally launched next month at the Sibos conference in Geneva, is to foster engagement amongst the global fintech ecosystem, share best practices and standardize knowledge and build bridges for greater collaboration between fintech hubs. The hubs will be ranked taking into consideration various criteria, including the amount of capital available, the ease of starting business, the talent pool available in the area, and how financial technology is regulated. The aim of this should not be to make them compete with each other, but to benchmark the best practices in order to grow the entire federation. GFHF will be funded with sponsorship from professional services firms and every member will potentially have the possibility to lead the federation as the plan is to have an annual revolving chair. Read more on Crowd Valley News!  |

AboutEst. 2009 Grow VC Group is building truly global digital businesses. The focus is especially on digitization, data and fintech services. We have very hands-on approach to build businesses and we always want to make them global, scale-up and have the real entrepreneurial spirit. Download

Research Report 1/2018: Distributed Technologies - Changing Finance and the Internet Research Report 1/2017: Machines, Asia And Fintech: Rise of Globalization and Protectionism as a Consequence Fintech Hybrid Finance Whitepaper Fintech And Digital Finance Insight & Vision Whitepaper Learn More About Our Companies: Archives

January 2023

Categories |

RSS Feed

RSS Feed

|

Digital Intelligence Globally

|

© 2009-2023 Grow VC Operations Ltd. All Rights Reserved.

|