|

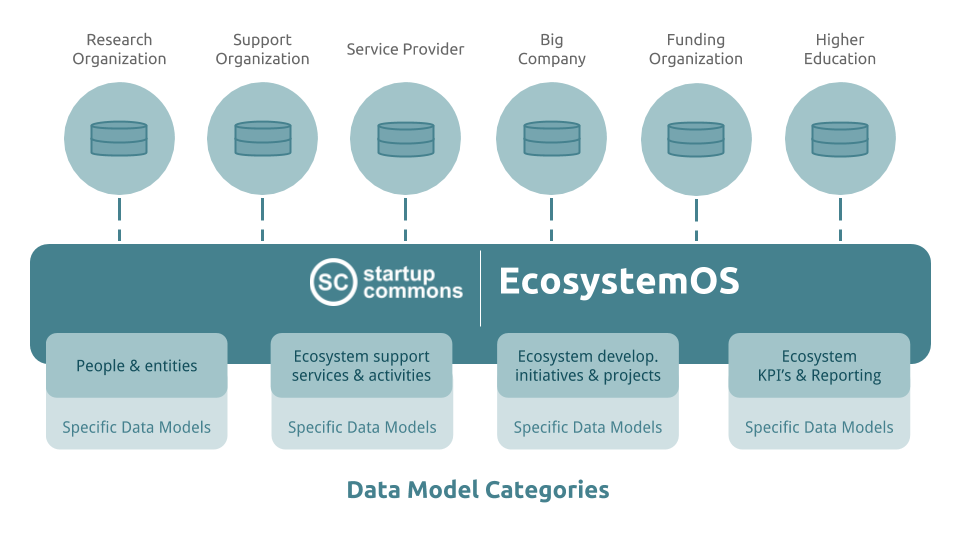

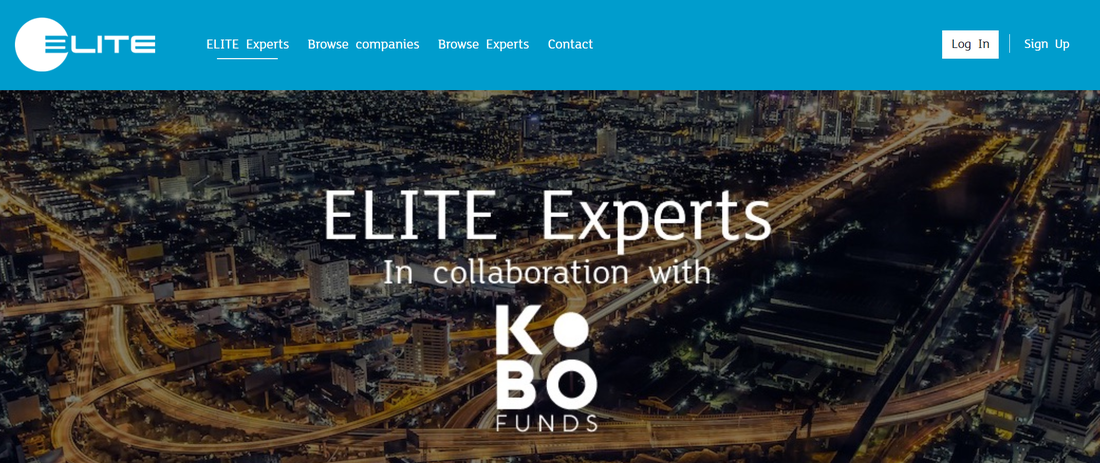

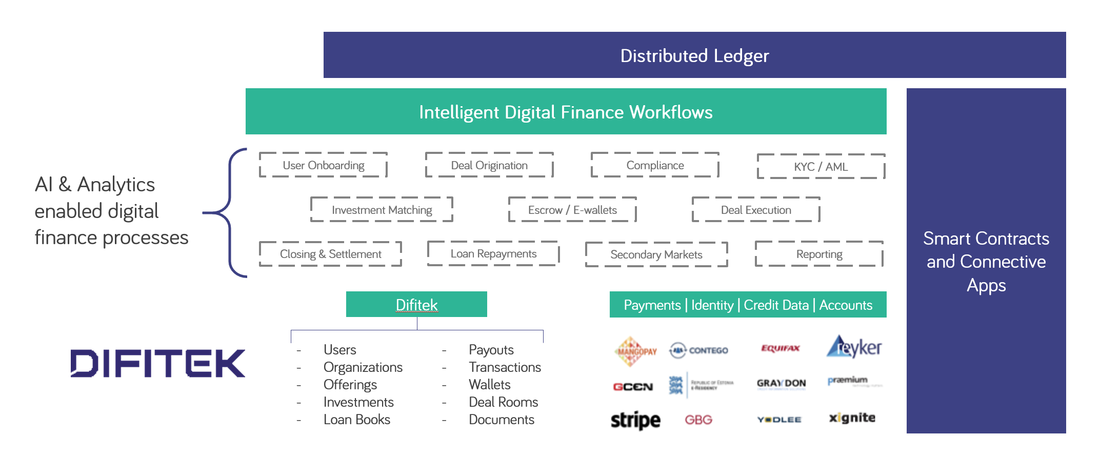

Startup Commons, a global platform for startup ecosystem development publishes its serverless service architecture - EcosystemOS. Startup Commons (a Grow VC Group company) launches its serverless platform version for digital startup ecosystem development and marketplace for application developers for sharing and distributing best applications and services between ecosystems around the world. EcosystemOS offers common user accounts and API's with documentation for user data portability, API connections, data models and data sharing principles to develop applications for startup ecosystems. It also includes a marketplace for connected ecosystem applications and third party API functions. EcosystemOS is especially used by public sector organizations (e.g. regional and municipal development agencies) and private startup services that operate startup and entrepreneurship ecosystems and offer services to startups, investors, and other stakeholders. “As part of our work with various startup ecosystems around the world we have come across with active interest to use applications from other regions and to learn from other application and SaaS service developers for own local ecosystem needs.” - says Oscar Ramirez, CEO, Startup Commons Global and continues, “While Startup Commons focuses on developing and providing EcosystemOS as the backbone for ecosystem user accounts, API’s, data models, data portability and sharing, we know there are many great applications and online services developed and validated in real ecosystems around the world. Now we want to offer an easy way to offer these applications globally through EcosystemOS. There are many excellent and dedicated developers that implement applications for startup ecosystems locally and have great understanding of unique aspects, challenges and needs of those ecosystems and startups in different phases. Now they get an opportunity to offer their services globally.” Learn more at: www.StartupCommons.org/EcosystemOS.html Contact Details Oscar Ramirez, CEO Phone: +34 656 180 880 Email: oscar@startupcommons.org Web: www.startupcommons.org About Startup Commons Startup Commons is dedicated on digitizing and connecting startup ecosystems globally to scale entrepreneurship, innovation and business creation around the world, by providing digital connectivity and solutions to enable data-driven economic development and policy making for local ecosystems.  ICOs and cryptocurrencies became a big thing last year. Some people think they have changed the whole world, while others think they are the biggest bubble we’ve seen in a long time. The value of an individual coin or currency is hard to evaluate when the market is new and transparency not always good. It is much easier to say that the concepts, models and technologies behind cryptocurrencies will make a big change for finance and also for the Internet and economies. Distribution, tokenization and tokenomics are the new new economy. Tokenization is the process of converting the rights of an asset or a service into a digital token typically on a distributed ledger such as blockchain. ‘Tokenomics’ is a model of distributed ledger-based financing for the economy. There are probably other ways to define these new terms, but basically, they refer to how securities and transactions can be based on digital tokens that are issued, sold and traded in blockchain-based markets and services. Note that these models and concepts are not important only for finance and FinTech. Distributed models are also changing the very fundamentals of Internet services. While Internet architecture is of course distributed, Internet services are highly centralized – big databases and services that gather a lot of users. This has led to the idea that the Internet easily creates natural service monopolies similar to Facebook, Google and Amazon. Blockchain and other distributed ledger models enable decentralized services in which data, transactions and ownership are distributed around the Internet to different parties. Bitcoin is a well-known example of this. It is not issued by a central bank, big banks do not handle transactions, and they are not stored in bank accounts. But this is not limited to virtual coins. Distributed models can also mean, for example, that each consumer owns and manages his or her own data. Currently big Internet companies possess and control the data – when you go to use a service, you log in, and the service provider uses the data it has collected about you to provide the service. In the future, you could come to the service provider and bring your own data with you (or an ‘avatar’ based on your data), and sign up for services based on your personal profile. This means, for example, you could apply for and receive an optimal loan using your own data via an API without relinquishing that data. Or it could mean a social media service doesn’t own or keep user data, but rather each user has his or her own data and updates – the social media service becomes just an API-based service that displays selected data to selected friends. Almost anything tradeable can be a token Tokenization has become relevant now especially for startups and new projects that have create utility tokens to use new services, security tokens for equity, and some hybrid models of security and utility tokens. The problem with many ICOs is that the tokens for these services and assets haven’t enough data to properly define a value for them. Tokenization can be done for all kinds of assets and services, and can be easier to value than startup equity. The ‘tokens’ could be real estate ownership, the right to live in an apartment, the right to use certain infrastructure, ownership of a private company, a currency issued by a government, or loyalty points from a supermarket or airline. Basically, all money, securities and vouchers can be digital tokens. This will change how we issue, sell and trade them. It will be all digital and it can be stored in blockchains, without a lot of paper work or central parties to handle transactions. Tokenomics is a new term that tends to be used in different ways in different contexts. Put simply, it means economical and financial models that use distributed finance and tokenization as the basis of the economy. It means digital tokens, blockchain, smart contracts and models without centralized transactions or authorization. As the Internet of the 1990s started to create big services and databases, tokenomics can distribute services, data and transactions. It is early days, of course, so it is hard to say now what all this means for businesses on the Internet. Right now we are worried that Facebook, Google and Amazon know more about us than we know ourselves, and they’re starting to manage our whole lives. Could it be that distributed models will stop this development and actually turn it in the opposite direction – perhaps to the point of even killing some Internet giants? At the same time, it is a threat for traditional banks, payment processors and even governments who worry at the loss of centralized control. Bitcoin, cryptocurrencies and ICOs are exciting and quick money for some people, just as some hot companies were during the dotcom boom in the late 90s. But these should not distract from the much larger and more fundamental developments happening behind the scenes that are going to change Internet services, finance services and traditional economic structures. It is not yet visible in mainstream activities and discussions, but many parties are already building those new structures, and the potential for disruption is massive.  Amazon can already recommend you books and movies, and remind you that it is time to order more coffee or toilet paper. Many other services make recommendations for you. In these cases the service or online store has your data and makes recommendations. But we are approaching an era where you can have your own data and your AI that makes purchases your behalf. It will change the customer experience, purchase decision making and the balance of power between stores and consumers. Now large companies, like retailers, banks and media companies especially own that data. They use this data to advertise, make recommendations and tailor offers to you. It is always in their hands to manage this process and optimize offers so that they can generate maximal value from you. Most companies use a lot of money to build their brands, image and appeal to the feelings of consumers. It has been important – a consumer's feelings and image of brands definitely have an impact on purchasing decisions. Actually, brand versus data oriented marketing practices have divided marketing people and departments, some marketing professionals believe much more in brand marketing and some others in data oriented targeting and optimization. In the future this can be very different. When you have your personal data and you can use engines (you can call it AI, personal assistant or data analytics) that actually make purchase decisions and orders for you. A good purchase assistant cannot only compare prices; it should know other qualities that are important to you in order to find the right products. It will definitely change a lot in terms of how retailers and other services offer their products, conduct their marketing, and offer data from their products. We have two very opposite developments in internet services at the moment - one that is its very early phase, and another that is approaching its peak. Big internet giants, retailers and finance institutions are becoming bigger, with more and more of your data that they can use to win more market share. Some people even see that Amazon is already so powerful in the US that it should be split based on antitrust laws. But this development can soon reach its peak. The new development in the internet is more distributed solutions. We have seen this especially with blockchain and cryptocurrencies. There is no central party or database to manage the data and transactions. This has started to have an impact on finance and especially fintech services. But it is not only limited there. Distributed models will change many other things on the internet, including retail, data management and ownership, and who and how to utilize data to make decisions. There are old IoT visions, such as how your fridge in the future will know what food you need to buy and make an order. It is hard to say, if it is a fridge or some other systems that will really start to do it, but this day is approaching rapidly. The fundamental change is when can you have your own data and engine to make decisions and orders, not simply trust the analytics of a store. We already have services that help e.g. to find flights, hotels, and loans based on your preferences. Especially with travel booking these services are significant. They are still quite manual services, when you need always fill your preferences and the compare different options, and some booking services even try to complicate comparisons by having additional attributes and secret prices that the comparison services cannot handle. Most probably there will be always some purchase decisions we want to make personally. At the same time, there is a significant part of purchases and orders we would like to delegate to a machine. A lot of data is already available to enable this, it just needs some new solutions that consumers can manage and utilize their own data and some smart machines to start to make decisions and send orders. It will put retailers and services into a totally new position. It is not enough to optimize offers and customer experiences only for human beings, but also for smart machines that have a lot of data. Maybe we will see an arms race between selling and buying machines and who have better data. Consumers get better AI that optimizes their purchase decisions and value for money, and retailers, finance services and other vendors have machines that target to maximize sales and profit. Regulation, like General Data Production Regulation (GDPR) in EU, has also an impact on this, when it empowers consumers to control his or her own data. It will be one more area where data is prevalent in the business in the future. The article first appeared on Telecom Asia.  Difitek's (a Grow VC Group company) customer APT Systems made announcement about new services and how its going to use Difitek's cloud based finance back office services. See the full release below. -- SAN FRANCISCO, CA , Feb. 05, 2018 (GLOBE NEWSWIRE) -- APT SYSTEMS, INC. (OTC Pink: APTY), a fully reporting public company in the Fintech sector, is pleased to announce that it has formally engaged the services of Difitek, Inc. to build the Verifundr escrow and payment platform. We look to Difitek to provide us with a modern framework, architecture and bank grade security features. The Difitek platform and API is currently used to build online platforms and marketplaces globally all with a view to managing private placements, securities, real estate, crowdfunding, peer-to-peer lending, and utility tokens. Their expertise will support Verifundr objectives and all projects currently on the table and more importantly, the Intuitrader trading platform as well. “We are excited to build our own unique digital finance marketplace and now, over the top to work with the team at Difitek, the newly branded operational arm of Crowd Valley Inc.,” says Glenda Dowie, CEO of APT Systems, Inc. “Their expertise is needed in all areas of our operations and we thrilled to have them officially on board after months of discussions.” RCPS Management, Inc. was created as a subsidiary of APT Systems, Inc. to allow management to explore and build financial systems. Verifundr, through collaborations, will provide escrow and transfer services to clients both bankable and the unbankable that run legitimate operations. Last year we joined the Ethereum Enterprise Alliance Network and will seek their expertise and input when developing our smart contracts that allow parties to complete agreed upon terms successfully and safely. We employ Blockchain ledger technology where it can enhance the security and history of transactions undertaken on the platform. To learn more, visit our website at www.verifundr.com. About Difitek: The digital finance company, Difitek Inc, provides the end to end infrastructure needed to launch digital banking and online finance products and services that are accessible through a single on-line interface layer (API) and supported by our highly scalable cloud back office. Today supported platforms are in use worldwide utilizing our core features: security, robustness and trust. About APT Systems: The Management of APT Systems, Inc. works to deliver stock trading tools like Kencharts and its platform Intuitrader, with a focus on handheld devices, while also strategically acquiring other compatible financial businesses which demonstrate strong growth potential. We are continuing our diligent search for software products that would enhance our operations while still watching dialogue on the proposed legislation for the Fintech National Banking Charter. Management launched its subsidiaries SNAPT Games, Inc. and RCPS Management, Inc. to further facilitate new financial products and long-term goals. Disclaimer: This press release contains "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and such forward-looking statements are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. "Forward-looking statements" describe future expectations, plans, results, or strategies and are generally preceded by words such as "may," "future," "plan" or "planned," "will" or "should," "expected," "anticipates," "draft," "eventually" or "projected." You are cautioned that such statements are subject to a multitude of risks and uncertainties that could cause future circumstances, events, or results to differ materially from those projected in the forward-looking statements, including the risks that actual results may differ materially from those projected in the forward-looking statements; projected events in this press release may not occur due to unforeseen circumstances, various factors, and other risks identified in a company's annual report on Form 10-K and other filings made by such company. APT Systems, Inc. (APTY) may opt to disseminate information about itself, including the results of its operations and financial information, via social media platforms such as Facebook, LinkedIn, and Twitter. Contact: Glenda Dowie, CEO 415-200-1105 Email: info@aptsystemsinc.com On Twitter follow @APTYsys Investor Online Info Kit: http://www.aptsystemsinc.com/online-investor-kit-for-apt-systems-inc-apty/  The Grow VC Group has decided to write off its ownership in Deal Index Limited. London based company, Deal Index, aggregated data from crowdfunding and alternative lending services. The target was to become a leading data provider in the market. The market didn’t become significant enough and we also learned the whole data market needs a change. The Grow VC Group was involved in Deal Index since 2014. The company managed to become, for example, the crowdfunding index provider for CNBC in Europe and Asia. The crowdfunding, but also p2p lending, markets development didn’t manage to meet our expectations all the while the fintech and alternative finance market otherwise grew very rapidly. Crypto finance has also changed the market. We also learned that models to focus to aggregate a lot of data and then try to monetize it are becoming more challenging. Many parties try to protect their own data, and Deal Index was not able to innovate quickly enough with business models. The crowdfunding market especially is also challenging to get reliable data and utilize it, when the companies are typically in an early phase and investments are less based on data. The Grow VC Group has been active to build and incubate new digital finance businesses since 2009. The market is developing so rapidly that we must learn all the time from the market and also be able to offer new and more innovative businesses and offerings. It is also fundamental to put focus and resources on companies and segments where we see enough growth. We have abandoned equity crowdfunding businesses and at the same time achieved a lot of success with technology and data solutions that can disrupt the whole finance market. Our latest company, Prifina, focuses on data in finance services. It totally changes technology and business models of traditional data business. It is based on distributed ledger technology models and it gives ownership and control of data to consumers and customers. We believe that distributed solutions are the future of the finance industry, they will change the whole industry and data business also changes significantly from centralized data models where big players try to aggregate and monetize all customer data, to models where customers are empowered with their own data. More information: Jouko Ahvenainen, jouko@growvc.com  The Financial Times, in partnership with IDA Ireland, presents the third edition of the European Financial Forum, bringing together international and Irish industry executives, policy makers, regulators and thought leaders to explore the disruptive forces that are shaping the financial sector into the future and discuss where opportunities lie. The forum takes in Dublin on January 31. The European Financial Forum will build on the success of previous editions and provide a fresh perspective the crucial issues impacting the financial industry today, including its role, priorities, drivers of growth and competitive environment. Through a combination of keynote addresses, on-stage interviews and panel discussions, this high level event will discuss the current geo-political and financial climate and the latest macroeconomic and regulatory scenarios. The participants in the invitation only forum are senior decision-makers and professionals working in banking, insurance, institutional Investment, asset management, financial regulation, economic research or policy, and FinTech. Grow VC Group Co-founder and Chairman Jouko Ahvenainen has been invited to participate in the forum. His interests in the event are especially discussions about FinTech and how it is linked and impacts on finance services as a whole.  Kobo Funds, the international investment network which connects global business professionals to entrepreneurs and investors, and ELITE, London Stock Exchange Group’s business support and capital raising programme for high-growth companies, are pleased to announce the launch of ELITE Experts, an added value service that will enhance the ELITE digital platform offering for ELITE Companies, giving them streamlined access to worldwide experts to support their growth journeys. Kobo Funds uses Difitek's (a Grow VC Group company) cloud finance back office for its platform. Group VC Group's Chairman Jouko Ahvenainen is also a member of the ELITE Exports program. Mr Ahvenainen comments the partnership, "It is great to follow the success of Kobo Funds. It is Difitek's important customer, and also a good example, how the cloud based finance back office enables new innovative finance services. It is also a great honor personally to be a member of ELITE Experts. It is really a unique group of top level finance professionals and business executives." See below the press release of Kobo Funds and London Stock Exchange Group in English and Italian. -- London, UK, 25 January 2018: Kobo Funds, the international investment network which connects global business professionals to entrepreneurs and investors, and ELITE, London Stock Exchange Group’s business support and capital raising programme for high-growth companies, are pleased to announce the launch of ELITE Experts, an added value service that will enhance the ELITE digital platform offering for ELITE Companies, giving them streamlined access to worldwide experts to support their growth journeys. Since 2012, ELITE has been on a mission to foster SME growth through accelerating company access to capital, while Kobo Funds has been pioneering the digital networking space since 2013 to match industry knowledge with financial resources. This strategic partnership is the outcome of their shared goals to provide ambitious companies with the assets they need to realize their growth strategies and adds to the suite of services available to ELITE’s ecosystem of companies, investors and advisors. ELITE Experts will be built by selectively engaging Kobo Funds’ global community of over 130,000 senior executives, industry experts and business angels and will be open to C-suite applicants with minimum 20 years experience in business and a successful track record. ELITE Experts will work with ELITE companies in three main areas: corporate governance, international development and financial management. Alessandro Tosi, founder of Kobo Funds, said: “We are proud to announce a partnership with an institutional player like ELITE, open to innovation in both fintech and professional networking markets. ELITE Experts represents the ideal digital venue for high-calibre business leaders keen on interacting with the fastest growing companies and the broadest community of investors. Top-tier executives have already joined ELITE Experts, acknowledging its uniqueness as the first professional community operating in partnership with a leading international Stock Exchange, where they can leverage their competencies, share their knowledge and embark upon a high-quality networking experience”. Luca Peyrano, CEO, ELITE, said: “Partnering with Kobo Funds is another achievement in the evolution of ELITE, allowing some of the fastest growing companies across the world streamlined access to an extensive network of business experts, ELITE Experts. We look forward to working with Kobo Funds and supporting ELITE companies achieve their enormous growth potential.” For further information please contact media@kobofunds.com and visit kobofunds.com/elite About Kobo Funds Founded in 2013, Kobo Funds is a digital platform matching companies and investors with an international community of experienced industry experts and C-level executives: more than 130,000 business leaders providing knowledge and support to entrepreneurs on their journey towards capital markets. -- Kobo Funds ed ELITE, società del gruppo London Stock Exchange, annunciano una partnership strategica Londra, UK, 25 gennaio 2016: Kobo Funds, il network internazionale che connette manager di lunga esperienza con imprenditori e investitori, ed ELITE, la società del London Stock Exchange Group, la cui missione è supportare le aziende nei loro progetti di sviluppo offrendo accesso ad un network internazionale, un percorso di mentorship dedicato e a fonti di finanziamento diversificate facilitando l’accesso ai capitali attraverso l’impiego di tecnologie digitali, sono lieti di annunciare ELITE Experts, un nuovo servizio a valore aggiunto che arricchirà l’attuale piattaforma digitale dedicata alle aziende ELITE offrendo loro accesso diretto a una rete di esperti internazionali a supporto dei loro piani di crescita. Dal 2012 ELITE ha come missione la crescita e lo sviluppo delle aziende facilitandone l'accesso ai capitali, mentre Kobo Funds è attiva dal 2013 come piattaforma di networking digitale, favorendo l'incontro tra competenze industriali e settoriali e risorse finanziarie. Questa partnership strategica è il risultato di obiettivi condivisi, che consistono nel dotare aziende ambiziose degli asset necessari a realizzare le strategie di crescita, e aggiunge un importante elemento ai servizi fruibili dall'ecosistema di ELITE, composto da aziende, investitori e advisor. ELITE Experts verrà costruita coinvolgendo in maniera selettiva la comunità globale di Kobo Funds - più di 130.000 executive di grande seniority, esperti di settore e business angel - aperta a top manager con esperienza almeno ventennale e con percorsi professionali di successo, interessati ad affiancare le aziende ELITE in tre aree principali: corporate governance, sviluppo internazionale e finanza d'impresa. Alessandro Tosi, fondatore di Kobo Funds, ha commentato: “Siamo orgogliosi di annunciare una partnership con una realtà istituzionale come ELITE, aperta all'innovazione nei mercati del fintech e del networking professionale. ELITE Experts rappresenta il punto d'incontro digitale ideale per business leader di alto profilo interessati a interagire con aziende in crescita e con la comunità internazionale degli investitori. Ad ELITE Experts hanno già aderito executive molto visibili, riconoscendo l'unicità della prima comunità professionale gestita in partnership con una delle maggiori borse internazionali, dove sarà possibile valorizzare le proprie competenze, condividere conoscenza e fare networking di qualità". Luca Peyrano, CEO di ELITE, ha commentato: “La partnership con Kobo Funds è un altro traguardo nell'evoluzione di ELITE, che offrirà alle aziende accesso a una rete mondiale di esperti industriali e di settore, gli ELITE Experts. Il progetto sul quale lavoreremo con Kobo Funds ci permetterà di supportare le aziende ELITE, caratterizzate da alta qualità e una forte propensione alla crescita a sviluppare ancor di più il loro enorme potenziale in logica sinergica con la community che già oggi fa parte della piattaforma ELITE ”. Per ulteriori informazioni si prega di contattare media@kobofunds.com e visitare kobofunds.com/elite Kobo Funds Fondata nel 2013, Kobo Funds è una piattaforma digitale che mette in comunicazione aziende e investitori con una comunità internazionale di esperti di settore e top manager: più di 130.000 business leader disponibili a offrire la propria competenza ed esperienza agli imprenditori che si affacciano al mercato dei capitali.

Grow VC Group and its companies participated in Crypto Funding Summit in Los Angeles on January 24 and 25. Crypto Funding Summit is a two-day event being curated by crypto enthusiasts, with an audience of about 500 people in the Los Angeles Convention Center. The summit gathered an interesting combination of people from traditional finance executives to startups, FinTech companies and crypto market investors.

Grow VC Group Co-founder and Chairman Jouko Ahvenainen spoke at the event. In his speech "Crypto Investment Ecosystem with Data and AI" he especially highligted needs for basic finance ecosystem components in crypto investing, and the fundamental changes distributed models will cause. He explained, how tokenomics, tokenization and distributed models change many fundamentals in the finance and Internet businesses. It is also a big challenge for many incumbent companies like banks and traditional data and Internet companies. Mr Ahvenainen also participated in a panel discussion "The Rise of Crypto Funds." A few Grow VC Group are also active to develop solutions for crypto funding, distributed finance, and fintech data services. For example, Difitek is the leading cloud based finance back office as a service, and it is used also for blockchain based finance services. Prifina develops new solutions for consumers to manage their personal finance data and use it in different services based on distributed ledger technologies. Token Index Fund is an investment company that invest especially in qualified crypto tokens and help other parties to make tokenization for their their assets.

With the advent of PSD2 in Europe, financial services companies have embarked on their Open Banking initiatives, which are set for full swing in 2018. Banks have been writing and exposing APIs for third parties to pull data and perform actions on the banks platforms through these APIs in order to provide more customer facing service innovation. For many banks this is the final step for complying with the PSD2 regulation, but the reality is that it’s only the very first step in the total transformation to an open financial services ecosystem. I had the pleasure of speaking at Google’s and Apigee’s CIO Summit on Ecosystem Strategies and showcasing our experience in financial services. Equally I was fortunate to listen to the presentations and the Google / Apigee teams fantastic work. It was extraordinary to hear first hand accounts of how large enterprises such as Pitney Bowes and Walgreens had adopted an ecosystem strategy and seen a vast return on their investment. This wave is now truly setting its sight on financial services. Connecting to the Ecosystem Exposing APIs is a way to allow third party access to data and actions on the banks systems, connecting to a community of service providers and ecosystem partners. These connections can yield fantastic new innovative services, such as we’ve seen in the first fintech wave with e.g. payments innovation, yet through the lateral exposure of new banking API platforms, these innovations will not be limited to one vertical and indeed over time they will impact every single financial services vertical application. This new position is, well new and with it these infrastructure provider and value add service provider relationships will be forged, yet no one knows what it will look like yet. What’s for certain is, that there will be a lot of new experimentation and the end users will get to play a part in shaping the future of financial services through their usage of newly created financial service offerings. Becoming a True Enabler As with any ecosystem strategy, these technical APIs need to become more than technical functionality. Ultimately the mere connection does not make the initiative valuable, but the potential the APIs provide for the third party ecosystem to ultimately together better serve the end users. The focus on value generation should be on the end user of financial services, the ordinary people and the quality of services they are offered directly and indirectly. Yet it’s important to recognize the vastness of financial services and that these applications range from life insurance products to car leasing and health care financing. But unless the end client consuming this service, for example the efficient financing of a vehicle purchase through increased competition, experiences that value in the most tangible way, such as better service, value for money etc, the revolution itself will be short lived. Or in fact, the model for the revolution would have been wrong. There’s a pervasive question at the heart of modernization in financial services, which goes something like this. There are two competing forces, 1) the modernization of financial services such as banks and 2) the re-writers of services, such as developers and larger software companies (Google, Oracle, Amazon…). In a give and take, who will take the most and who will give the most? Where does the balance sit in five years, how about in ten? Not One Wave, but an Ocean This vastness in financial services, including the fact that there is an inherent depth to each vertical of added dimensions (regulatory, domain expertise, scale needed etc) means the shift will not be one wave of change, but rather a series of waves that will gradually shift the entire services market. Adopting an ecosystem strategy will take time, but the time is now. Keeping a direct focus on the end user value, we look forward to welcoming adopters of ecosystems strategies to the open market as well as the innovators writing new code to serve clients in a new way. This second wave of fintech has got to include you all. The article first appeared at Difitek Blog.  Again there is speculation in the US over whether companies like Amazon, Facebook, Apple or Wal-Mart could acquire a banking license. The tradition in the US and many other countries has been that lawmakers and regulators have wanted to keep banks separated from other businesses, like retail, as it could for example create conflicts of interest in terms of making lending decisions in purchasing the company’s own products. Whatever happens about this regulation, thanks to FinTech, we’ll see more finance services integrated with other services. If you go to buy items online, you might need finance for your purchase. The easiest solution nowadays is probably to use a credit card to make the payment. Then, depending on your card, you have more time and flexibility to make the payment. The problem is the actual annual interest rate of the card is easily 30% to 40%. You could get a loan with much lower interest rates, but it is complex to get a loan quickly when you are buying something. Some services offer you ‘financing models’. For example, you can buy a mobile phone by taking a two-year contract with a carrier. Those packages then typically include some call time, text messages and data. As a whole those pricing packages are often complex and it is difficult to calculate how much you actually pay for the phone and what is your interest rate is on the deal. FinTech solutions distribute the whole finance industry in many ways. There are more niche services for lending, investing, savings and many other needs. We are moving from a model where a few finance institutions were big black boxes offering all services to a network of countless smaller services with open APIs. An important part of the new services is better usability. You don’t need to go to a bank branch to apply for a loan and take your ID card, utility bills and bank statements with you. You can create an online application in a few minutes and systems based on data analytics make the lending decision and pricing in real time. Now it is also easy to build these kinds of services technically. There are finance back office services, development components and open APIs available, and it is possible to implement a service in a couple of weeks. This also means that these kinds of finance services can be easily integrated to the check-out process of an e-commerce service. An e-commerce service can also integrate many lending services to their service offering, and a lending service can be integrated to many e-commerce services. It opens the market for open competition. In practice, this means a consumer could have a list of finance solutions on an e-commerce service, when she or he purchases something. She could compare which one is best for her needs, receive financing on the spot and make the purchase. This doesn’t mean that the e-commerce service offers the finance services or is a finance company. They just make those services available on their web store as part of the ecosystem. Traditionally available finance has been an important part of competition, for example, in the car market. Many car companies have their own internal or external finance partners. When you have bought a car, it has always included some paperwork and the finance part has been an additional layer extra. But for smaller purchases that kind of paperwork would be too complex. Now we see a situation FinTech that integrated finance solutions are easily available for all kinds of retail services and they offer also a smooth customer experience. This is part of a much bigger development in the finance industry. Finance services are no longer their own isolated islands, but they can be components in any service. The FinTech discussion has still often been linked to some highlights like p2p lending, bitcoin or mobile banking. The reality is that the impact is much larger for the whole industry and how it works. It will also change how and where finance services are offered to people. For example, you need credit or a loan, but when you buy something, you just want to buy it, not to go to a bank or a lending service. When the services are truly built based on customer needs, it changes their availability and customer experience fundamentally. This post originally appeared on Telecom Asia.  |

AboutEst. 2009 Grow VC Group is building truly global digital businesses. The focus is especially on digitization, data and fintech services. We have very hands-on approach to build businesses and we always want to make them global, scale-up and have the real entrepreneurial spirit. Download

Research Report 1/2018: Distributed Technologies - Changing Finance and the Internet Research Report 1/2017: Machines, Asia And Fintech: Rise of Globalization and Protectionism as a Consequence Fintech Hybrid Finance Whitepaper Fintech And Digital Finance Insight & Vision Whitepaper Learn More About Our Companies: Archives

January 2023

Categories |

RSS Feed

RSS Feed

|

Digital Intelligence Globally

|

© 2009-2023 Grow VC Operations Ltd. All Rights Reserved.

|