|

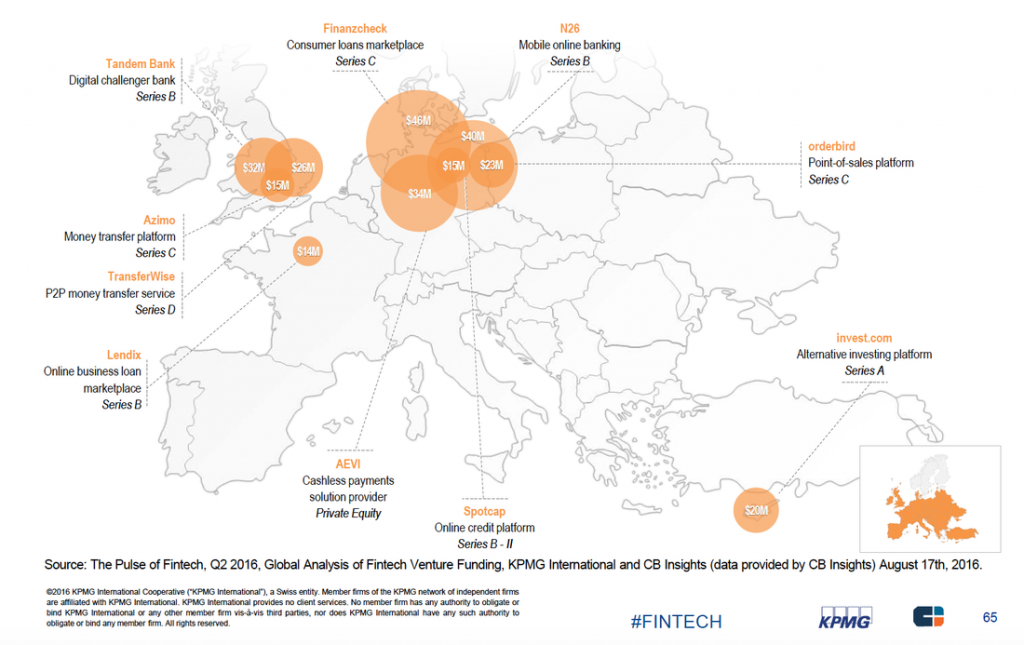

In the second quarter of 2016, the investments received by VC-backed German financial technology companies, have been 80% higher than those for UK ventures, and its fintech ecosystem is now growing at a good pace. According to a new report from CBInsight and KPMG International, in Q2 2016, the funding activity on fintech startups slowed compared to Q1, which was under all aspects a record quarter in North America and Asia. However that’s not applicable to Europe, where despite all the concerns of the Referendum vote, investments have grown again, with $369 million raised across 43 deals, and with Germany largely responsible of this increase, with investments that grew from $107 million in Q1 to $186 million in Q2. The UK paid for uncertainties of the Referendum vote, which now represents a challenge and an opportunity for the whole European market. We agree with Anna Scally Partner, Head of Technology, Media and Telecommunications, and Fintech Leader, at KPMG in Ireland, when she says that: “Market access and the ability to passport services across the EU are hugely important for fintechs, regardless of their origin or stage of development. Post-Brexit, maintaining a pro-business approach in Europe is critical and these issues will likely feature strongly in discussions between the EU and UK.” The industry is now growing and evolving, not just in Europe but all over the world. Germany is building up what it seems to be a solid financial technology ecosystem, with the appetite to involve key cities and not just a single location, and it is now well positioned to play a bigger role in the financial technology industry in the future. Read more on Crowd Valley News.  The benefits of technology applied to existing processes making them more efficient or effective should be very practical. However, it’s easy to get lost in over hyped terms such as ‘fintech’, ‘peer-to-peer markets’, ‘crowdfunding’ and forget what the practical benefit is. In this post let’s open up a few scenarios and walk through them step by step, to examine the applications of new technology in existing operations value chains and delve into the practical implications and value at different stages. To set the context, let’s imagine a private market lender with interests in setting up a digitalization strategy for the longer term and position their bank as a leader in the modern financial services market. To achieve this, the lender plans to open a sector specific marketplace where they will originate and lead deals, and invite other institutions with an interest to maintain a regulatory compliant profile, gain access to deal room to diligence and follow deals, with the option to participate in the syndication of these deals as a co-investor. Ultimately bring down the cost of capital, increase distribution and elevate the lenders corporate profile:

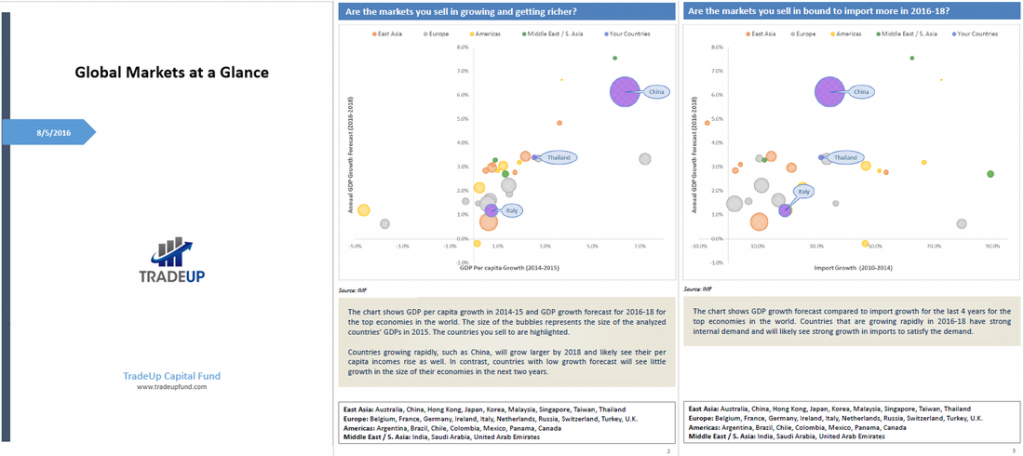

We’ve delved into a few different areas of impact that digital platforms can have in a digitalization strategy when employed by an institutional client, such as an asset manager or private market lender. The applications and impacts of digitalization strategies can be very tangible, and we encourage our clients and partners to discuss them and how they can benefit their organizations, rather than the general trends of fintech. Read more on Crowd Valley News.  “In the U.S., 33 percent of millennials (ages 15-34) believe that within next five years they will not even need a bank”. – McKinsey & Company. Global Payments 2015: A Healthy Industry Confronts Disruption. It is difficult to conceive a reality where banks stand redundant and, while the probability of such a happening is highly unlikely, a large number of individuals globally are adopting a new set of expectations for the infrastructure that supports their pecuniary activities on a p2p, p2b level, e-commerce, or for cross border transactions. While the efficiency of different complementary services may not be uniform across all sectors of banking and monetary transactions, with expectations having been established by more modernized sectors such as the payments sector [35% of fintech companies are active in payments sector (McKinsey)], consumers are increasingly putting pressure on banks and other financial institutions to put in place infrastructure that meets these expectations across the board for services like retail banking, availability of information, transparency, fraud detection and compliance (ID verification, KYC, Credit Review). Consumers are also becoming noticeably more independent when it comes to their financial decisions. Even in terms of advice from financial services firms, they don’t want to talk face to face with an advisor but they want to feel special & have the ability to switch seamlessly between personal and hands-off options. These are no meager demands to place on a traditional bank whose entire infrastructure requires significant investment in data and analytics capabilities (McKinsey) to support these demands. As Eli Broverman, Co-Founder and CEO of Betterment explained “In some cases, investors want to self serve, but they want to self serve in a different way than they have traditionally self served. They want that advice in a digital format.” To succeed, financial institutions will need to dramatically increase their customer insights and understanding allowing for a tailored and unique experience for each customer interaction. As customers grow accustomed to faster and more convenient payments on the retail side, they will soon demand similar conveniences and service levels in transaction banking as well (McKinsey). As consumers grow accustomed to the benefits of using technology in their daily lives, their expectations also grow. Nonbank digital entrants have used superior design and user interface to build solutions that often surpass consumer and merchant expectations in terms of end-to-end customer experience. By integrating payments into commerce, nonbank attackers have created more seamless, personalized and interactive experiences, contributing to increased conversion rates (McKinsey). The one aspect that the traditional banks have in their favor is the vast amounts of data being collected and stored, which banks can use to develop insights on consumer behavior and maybe even get ahead of the curve. As of now though, it’s a catch up game; Banks’ core platforms will need to be updatable in real time, fraud platforms and processes will need to be very near real time, and clearing systems must be capable of handling exchange of information, posting of transactions to the customer and funds availability all in real time. Or face being left behind in this new form of disruption the industry is facing. Read the whole article on Crowd Valley News.  Grow Advisors (a Grow VC Group company) publishes its daily insight into the world of alternative finance and fintech. Here are some highlights: Fintech & the challenge of changing innovation models Proof that fintech facilitates business and generates value can be found in the fast growing alternative finance sector. Digital technology has given financial service innovators tools that connect investors with those seeking funds. Constant improvements in user experience coupled with initiatives to create trust and security will provide future growth. Today, customers rely on mobile devices to manage their lives, and traditional financial service providers look to adapt or risk losing profit pools. 5 customer engagement principles fintech shouldn’t forget Fintech has become part of everyday lexicon of many in the financial services industry. Yet, while we let the technology consume our thinking, few discuss how it all started – customer needs. Far too frequently, we see how in the pursuit of technological advantage, clients leave customer engagement as an afterthought. For our team, it’s the starting point and the beginning of all discussions. Let’s address the imbalance. Read 5 core principles. In Fintech, the battle for customers’ hearts must go beyond competitive pricing The success and growth of online lending platforms has traditional banks concerned over the risk of market share erosion and profit losses to competitors. Goldman Sachs estimated the profit at risk to be US$11 billion out of a total US$150 billion in the next 5 years. We believe this was just the start, in an industry still in its infancy. Traditional banks are now busy developing differentiated propositions that will take the battle to a new level; the battle for the customer’s hearts and long term loyalty. Read more at Grow Advisors Blog.  Grow Advisors (a Grow VC Group company) publishes its daily insight into the world of alternative finance and fintech. Here are some highlights: Why the Wells Fargo debacle should worry many banks In September, Wells Fargo admitted to falsely opening millions of banking and credit card accounts over the course of 5 years, without customers’ consent. The bank fired over 5,000 employees involved in the misdeeds and handed a US$185 million fine. At the heart of the scandal is the stress managers were under to reach [unrealistic] sales targets. Former employees speak of relentless pressure and increasing quotas as the cause for their actions. Consider an alternative and worrying perspective: one that involves a fast changing landscape, reluctance to change, unmet consumer demands and the resulting revenue declines. The world’s financial centres regulate emerging fintech Technology and financial services firms developing fintech services face similar hurdles presented by old regulatory frameworks that were not designed to support digital business. Compliance is a fundamental and immovable base on which to successfully grow the fintech sector. At the same time, central banks and regulators realise they play a vital role in enabling innovation. While regulatory authorities maintain dialogue with counterparts around the world, it has been suggested that cooperation is limited as each country competes to attract business Online Lending – The Fintech Chimera The Chimera was, according to Greek mythology, a monstrous fire-breathing hybrid creature of Lycia in Asia Minor, composed of the parts of more than one animal. Innovation, like evolution, takes on many forms. Though always present in financial and investing services, in the last ten years the pace of innovation in all industries has quickened due to technology, regulation and customer needs. And when it comes to online lending, we are beginning to see an evolution in business models, as in-market experience begins to shape how businesses operate. The innovation will result in evolved organisations that take the best of both worlds. Read more at Grow Advisors Blog.   Startup Commons (a Grow VC Group company) co-organizes Connecting Globalizers and Localizers event in Singapore on September 19. The event is a Slush side event. Startup Commons organizes the event with KPMG Digital Village, Slush Singapore and Team Finland. “Connecting Globalizers and Localizers” is a “selection only” matchmaking event that aims to connect growth stage companies which are looking to scale their solution globally (Globalizers) and serial entrepreneurs or intrapreneurs (Localizers) who are looking to adopt existing innovative solutions from another region to start a new business venture within their local and regional markets in SEA countries. This event adopts an alternative approach towards internationalization by providing leading startups a platform to showcase their solutions with the aim of generating successful partnerships to drive the commercialization and adoption of proven products and business models locally. Commercial models could include, for example, a joint venture or the establishment of a new company which licenses or franchises the proven solution. GLOBALIZERS A Globalizer is a growth-stage revenue-generating company that has a proven business model and product who is looking to internationalize by partnering local entrepreneurs: 1. Your company has a market-validated product and business model 2. You are growing internationally or have international expansion plans 3. You are looking for local entrepreneurs or co-founder teams to build business in SEA countries 4. You are not just looking for partners, employees or resellers, but offering an opportunity for significant local equity ownership to potential partners. LOCALIZERS Localizers are serial entrepreneurs, experienced leaders or resident intrapreneurs who are focused on kickstarting new business ventures in their home/regional markets through the adoption of existing products and business models. Specifically, 1. You are willing to take an entrepreneurial risk to have an opportunity to build a local successful company for an existing product or service 2. You are looking looking to become the local CEO or be part of the founding team. 3. You have past entrepreneurship experience or have been responsible in creating and growing new businesses. THIS EVENT IS NOT for those who are simply looking to: – sell their products or services to others in the event, – find local resellers or distribution channels or – looking for investors. Ask more information from Startup Commons.  The Hong Kong Monetary Authority (HKMA) last week announced the launch of a financial technology sandbox, to allow banks to test new innovative products that do not yet meet compliance standards. The new regime is valid as of September 6. The announcement comes a few months following similar action by various governments around the world, including the UK, Singapore, Australia and France, but more recently also in other countries in the area, including Malaysia, Thailand and last but not least Japan. The main difference here is that the the regulatory sandbox would be not applicable to standalone fintech firms, but it’s only applied to banks. We believe this is a fundamental benefit, given the disruptive innovation being leveraged around the world in innovative banking institutions. This initiative is the third one in less than a year announced by Hong Kong. At the start of the year they established a fintech steering committee, before that the financial regulator announced, just two months later, an office to promote fintech through the organization of industry events. The good news of “Fintech Supervisory Sandbox” was brought by Norman Chan, Chief Executive of HKMA, in a keynote speech at Treasury Markets Summit 2016. Going further talking about the regulatory framework sandbox he says that it “allows banks to conduct testing and trial of newly developed technologies and applications on a pilot basis. Within the Sandbox, banks can try out their new Fintech products without the need to achieve full compliance with the HKMA’s usual supervisory requirements. Read the whole article on Crowd Valley News.  Sign up now for Global Markets at a Glance by TradeUp, a free tool for companies expanding abroad. TradeUp is committed to helping SMEs and startups raise the growth capital they need to get into markets around the world.

Sign up for your free customized report here. Learn more here.  Grow Advisors (a Grow VC Group company) publishes its daily insight into the world of alternative finance and fintech. Here are some highlights: The fast growing European Alternative Finance Market France, Germany and the Netherlands are the top three countries for online alternative finance by market volume in Europe, excluding the United Kingdom. The French market reached €319m in 2015, followed by Germany (€249m), the Netherlands (€111m). The Nordic countries collectively pulled in €104m, while Eastern & Central European countries registered a total of €89m. The UK still dominated the European online alternative finance landscape, increasing its overall market share of Europe to 81% in 2015 with €4,412m. 5 Themes Driving Digital Transformation in Banks

How organisation design can boost digital execution A common management expression you may hear in many operational situations is ‘execution trumps strategy’. In the digital world, we have seen this expressed as ideas are worthless; execution is priceless. Read more at Grow Advisors Blog.  This is not a soft question, it’s actually the most challenging one you could ask. It could be the key to creating a sustainable and thriving business. This question is relevant also for fintech services. Head of Vision at Grow VC Group, Alan Moore,is bringing his experience of how to craft beautiful businesses, when he helps companies to develop better business. The challenge to embrace what is real The search for beauty challenges you to see more deeply. By focusing on beauty you are not being soft or touchy-feely; on the contrary, you are demanding rigour and discipline. As philosopher poet Ralph Waldo Emerson put it, “Beauty gets us out of surfaces and into the foundation of things”. It’s not an escape from reality, but an intimate embrace of it. If your business were more beautiful… What would be different about its culture? Is it possible for a business to do workaday, mundane things, but still in a beautiful way? How would leadership work in a more beautiful version of your business? These are the sort of questions Alan is asked as he tours with his book - Do Design. Why beauty is key to everything. The book explores how the idea of beauty applies to businesses from high tech to axe-making. If you find these questions intriguing, please join us and others who do so too. We’ll be gathering to enquire, explore and create, together. You might be stuck in working out what direction to go in. Or seeking a more inspiring vision. Or trying to find new ways to make money. Or working out what your new technology can truly give to the world. You might be launching a precious new business, or working to rebuild an old one. Or a thousand other things besides. Read more and register here for a gathering in a beautiful old church in Bishopsgate, London.  |

AboutEst. 2009 Grow VC Group is building truly global digital businesses. The focus is especially on digitization, data and fintech services. We have very hands-on approach to build businesses and we always want to make them global, scale-up and have the real entrepreneurial spirit. Download

Research Report 1/2018: Distributed Technologies - Changing Finance and the Internet Research Report 1/2017: Machines, Asia And Fintech: Rise of Globalization and Protectionism as a Consequence Fintech Hybrid Finance Whitepaper Fintech And Digital Finance Insight & Vision Whitepaper Learn More About Our Companies: Archives

January 2023

Categories |

RSS Feed

RSS Feed

|

Digital Intelligence Globally

|

© 2009-2023 Grow VC Operations Ltd. All Rights Reserved.

|