|

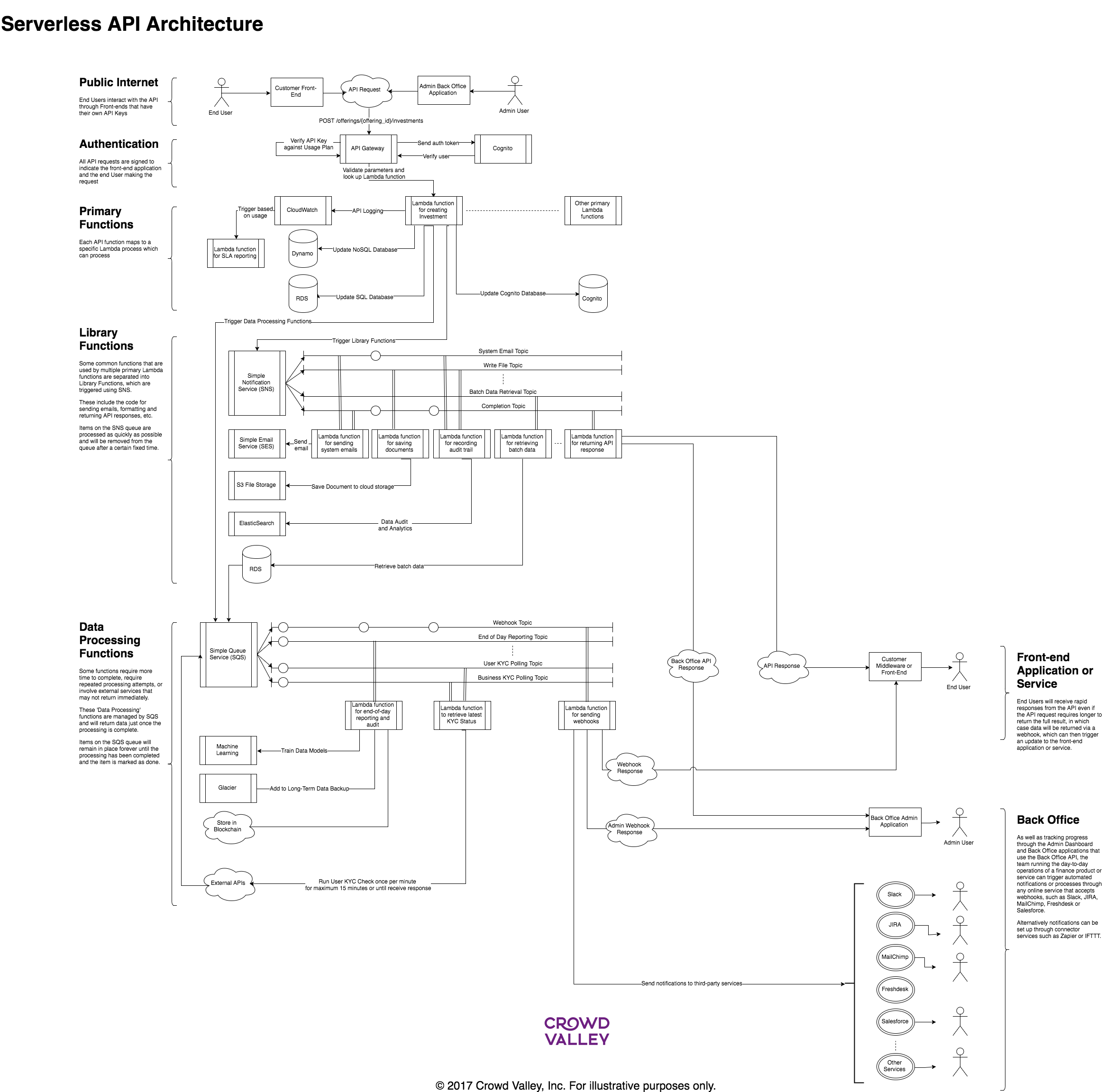

Clouds have become the standard for many online services. Now we are really moving to serverless services that offer many benefits over the traditional cloud server models. Serverless architecture can offer better use of resources, more cost-effective pricing and also better security against some threats. There are, of course, still servers in serverless solutions. Serverless means dynamic allocation of server resources, i.e. we don’t need to pay or rent dedicated servers, but we buy computing capacity and we can use it based on our needs. These solutions are also called Function-as-a-Service, FaaS. Most leading cloud providers already offer serveless services, for example, AWS Lambda, Google Cloud Functions, IBM OpenWhisk, and Microsoft Azure Functions. Serverless models also change software architecture. The microservices model means that each small task or job is a separate function that works independently. For example, in a finance service a KYC process (know-your-customer) can have an independent ID check, sanction list and anti-money laundering checks, so that all of them are independent functions that can run in parallel too (see an implementation example in the picture). This model enables the development of more independent functions by different developers and also makes it easier to debug smaller functions - and the same functionality can be then used for different services. Of course, starting and running many functions also creates some overhead, but it is quite small compared to the benefits. This doesn’t mean that all services need to become microservices, it is possible to also create functions that handle bigger tasks. Serverless means that a service provider needs to pay only for the capacity actually used. This is especially valuable for services where capacity needs vary. Earlier a service needed capacity based on peak demand, but with serverless models the service pays for the functions executed in the cloud service. These solutions neither take resources for traditional server setup or management work. The concept also makes it easier to implement API services that can process in the background and an API call doesn’t lock any other services. For example, a user can ask his / her investment portfolio details. The back office API replies immediately that it will be processed. The actual data then comes in several patches through webhooks to the front end. This can help also with blockchain implementations, when blockchain functions often don’t guarantee any latency time. The serverless model works very well for many digital services, but of course, there are still some services where the traditional server model is faster and more cost-effective. For example, services that constantly require a lot of computing capacity are probably better to run in the traditional environment to avoid the overhead required to constantly start tasks when capacity is needed. When the load is easy to predict, it is also cost-effective to rent an optimal server capacity. Most internet and mobile services have off-peak and on-peak periods. FinTech services are one example of those. If we think for example about payments, finance back office functions, and banking services, load needs vary a lot. They are also often critical services, i.e. they must work properly also during a peak demand. Serverless solutions can also offer better security against some threats. For example, a serverless solution is more immune against denial of service (DoS) attacks, when the service is not dependent on certain servers. An attack can create additional costs, if it means a lot of capacity is used for in-coming requests, and attackers with massive capacity can target a whole cloud. Some serverless clouds (at least AWS Lambda) offer tools to require API key or authentication for a function. This means a DoS creates only API calls to the API gateway, but don’t start more processing - this eliminates the load and cost effects of DoS. The model also helps against attacks that compromise individual servers that are then used to attack further. Serverless also eliminates problems caused by unpatched server software. This doesn’t mean all of this comes without any potential issues and security risks. Vulnerabilities in software and applications are still a risk. Serverless can also make traditional security monitoring more complex. As a whole we can conclude that serverless can help with security risks, but it also needs competence to manage vulnerabilities and a new kind of software and data architecture. FinTech is a fast-growing service area that is also moving to clouds. This is a good timing also consider serverless solutions for finance applications, especially when they can also help with security. You can already develop a serverless payment solutions with Stripe. Crowd Valley is piloting serverless version of its finance back office as a service. US bank Capital One has been reported to be an AWS Lambda customer. Thomson Reuters and US finance industry self-regulator Finra also already use serverless solutions. Serverless solutions will most probably come to dominate all event-based services. It fits well to financial services too, and timing with many other new things in finance is now good to make the transition. For example, the PSD2 regulation will open APIs to banking services and will significantly change finance services and their structures (read about old banking APIs). Serverless can offer a lot of value to create more cost effective and stable services, but of course they also need their own competencies to do it right. This post originally appeared on Telecom Asia.  Los Angeles & Hong Kong, September 29, 2017 – Grow VC Group, the leading fintech technology and data holding company, has today officially sold its ownership in Los Angeles based TradeUp Capital Fund (TradeUp). TradeUp offers efficient services for export capital. The new owners will integrate the offering into their existing portfolio of export services. The acquirer sees that new finance services for export business are an important part of a service portfolio to support export companies. The companies have decided to not disclose the acquirer or price. The acquirer will announce its future services later on in the year.

The Grow VC Group has been an owner in TradeUp since early 2014. TradeUp was the first online investment service that especially focused on companies that raise capital for globalization and export. Grow VC Group has been an owner and investor in several online investing and crowdfunding services since its inception in 2009, and over the markets maturity divested several ownerships, and focused on enabling technology and data in the fintech market, and increases its operations for blockchain, financial data and digital assets (including ICO) based solutions. Grow VC Group companies build businesses that enable digital finance services globally, by offering technology, data, finance instruments and competence to disrupt old finance models, and making it easier for anyone to implement new finance services, invest and get access to capital. Established in 2009 Grow VC Group is the global leader of fintech innovations, digital and distributed finance services, and digital infrastructures. Its mission is to make the finance services more effective, transparent and democratic. More information: Jouko Ahvenainen, Chairman, Grow VC Group, jouko@growvc.com, +1 646 363 6664 Grow VC Group and its companies will participate and speak in several FinTech events during the fall 2017. We listed here some events the group representatives will speak. The speeches focus especially on new digital finance services, data and data analytics, and enabling technology that disrupts finance services.  Hong Kong FinTech Week is a leading FinTech event in Asia. It combines the development of FinTech in the traditional finance hub Hong Kong, in the leading FinTech country China and the latest development in Asian emerging markets. Grow VC Group Co-founder and Chairman Jouko Ahvenainen speaks in the event and focuses especially on data, data analytics and AI in FinTech.  FinTech World event in Washington DC focuses on blockchain, digital currencies and new ways to have digital assets. This event gathers the leading digital currency and blockchain experts in the US. Grow VC Group's Jouko Ahvenainen speaks about data and AI for digital currencies and assets, and Crowd Valley's (a Grow VC Group company) Markus Lampinen about technology to build services, market places and applications for blockchain, crypto currencies and ICOs.  World Funding Summit in Los Angeles has the leading experts of the funding market to talk about new funding models, online alternative finance and how digital currencies, assets and ICOs change the market. An important theme is also, how these new solutions can make the finance market more equal and democratic. Grow VC Group's Jouko Ahvenainen speaks, how new solutions, instruments and digital assets change the fund raising and investing.

In many industries – such as airlines, retail, and media – disruption has been linked to new low-cost, almost commodity-type services. Southwest Airlines and Ryanair paved the way for low-cost flights, online news has become a commodity, and retail chains like Walmart, Aldi and Lidl have created a new cheap-prices-always category. The common theme is: cheap basic things, with a better experience available for a premium. FinTech disruption is changing finance in the same way, and when basic finance services become a commodity, they will be integrated to other services. Some finance services have, of course, been in this category for a long time already. For example, payments are a crucial part of all e-commerce services and brick-and-mortar check out processes. It has become natural that services use third-party payment solutions rather than develop their own. We will see the same development for many other traditional finance and banking services. Online lending, p2p lending and quick loans have been a fast-growing market. Those new lending services offer many benefits – sometimes a better price, but typically a much better customer experience. Sometimes they offer loans for people who cannot get a bank loan, and they might have more flexibility in terms and conditions. For many loan categories, bank loans are not a very attractive option anymore, especially when you factor in the customer experience, paperwork and time needed to get a loan. Ford Motor Company just announced that they are going to adjust their car finance process (read more on WSJ). They decided that the traditional credit-scoring model is not very effective or optimal nowadays, and that they could get more customers and sell more with new finance models. Basically, they plan to use more data from new sources to get a more accurate profile of customers and optimize their financing better. It’s worth noting they were forced to do this because alternative lending services are already doing it, and competitive finance is an important component in car sales. Car sales finance is just one example illustrating that companies outside the traditional finance sector need to develop better new finance solutions. FinTech makes it easier. The real estate sector has adopted a lot of new finance and investment models during the last five years, especially in the UK and the US – but now new real estate finance services are emerging globally. This means there are many new models available to invest in real estate – e.g. in development projects, rented apartments and commercial buildings, and new models to lend and borrow in real estate. Typically, this includes new finance instruments that are then offered through online finance services. These services are offered by some finance companies, real estate development companies and several startups. At the same time, more inexpensive technology – or even technology-as-a-service – is available to build finance services. You don’t need a $100-million-plus IT back office to set up an investment or lending service – you can get it as a service from cloud, and they can offer access to relevant data sources (including credit ratings and richer data). It is quite easy to develop the actual application and your own investing and lending models. We will see more:

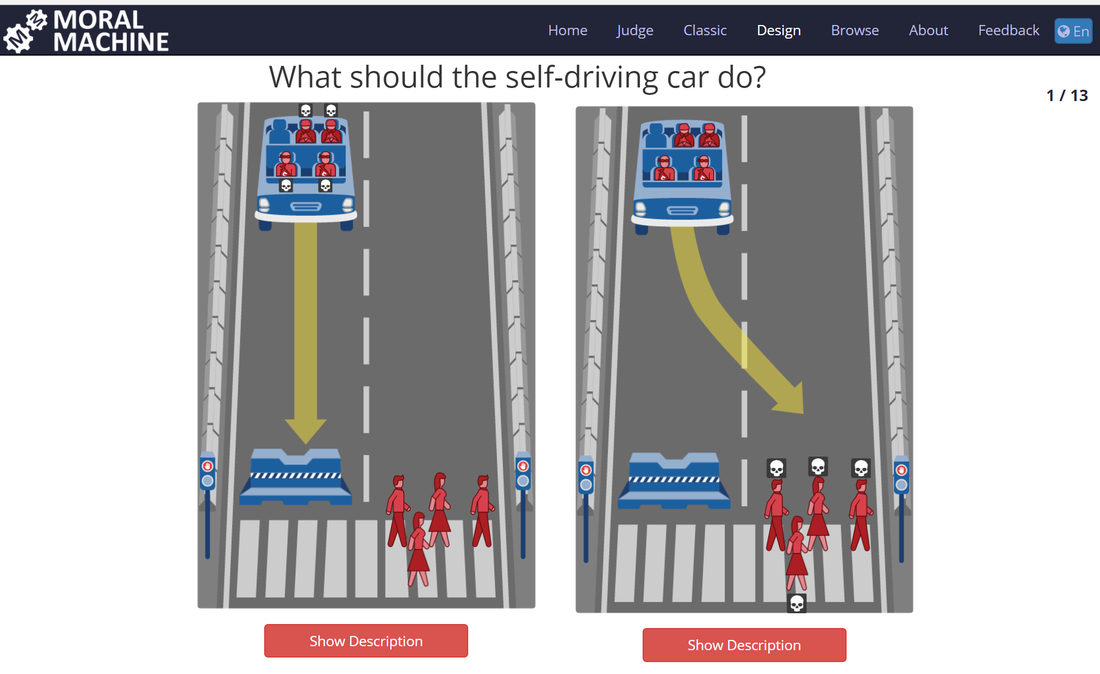

All this is a part of the overall development towards an API and platform economy. Finance is becoming an integrated component for many other services. It means more competition for banks. But it also means significant new competition for credit card companies that have had an important role in smaller online purchases, and their money has typically been expensive. When we think about FinTech and its impact, it is easy to focus only on the traditional finance sector. Certainly there will be significant impact on the whole finance value chain, as I have written earlier. At the same time, however, finance is shifting to a platform economy, and it is fundamental to adapt to the requirements of that business model by building the business network, offering APIs and utilizing data. After a few years, we will think about the old-fashioned bank loan process, with all these paper forms, and laugh as we do now at the thought of sending a fax or buying printed flight tickets. This post originally appeared on Disruptive.Asia.  Artificial intelligence (AI) and machine learning (ML) are becoming an infallible part of the development of present-day technology. Yet the public discussion often centers around a notion of a ‘human-like’ robot and my concern is that the impact gets downplayed. How then should we look at the future with AI? One way which may be helpful is examining the aspect of morality and consciousness, or rather, the lack of both in decision-making in a new paradigm. Humans have evolved based on a complex process of long-term trial and error. Our biological machinery has been honed over thousands of years to optimize (mainly) for survival and procreation and for these tasks, the human mind is highly advanced. However, we have to realize that the subjective aims of the human mind are the primary reason and motivation for all decisions made. Morality is a key element in the support of sustaining these two goals of the human species, and has successfully introduced a human-wide consensus to better our chance to achieve our goals. As we look at crafting AI for better data-driven decision making in critical processes – such as optimizing far-reaching and complex value chains, making real-time decisions in applications such as self-driving cars and many more – we should recognize that without coded in morality, AI will actually act without the concept of morality or human subjectivity. In short, it will optimize any and all decisions based on the rational best outcome for the desired parameters rather than what ‘a good person would do.’ A Future with Less Morality May Be One Humans Find Uncomfortable Looking at the grinding, long process of trial & error humans have undergone to evolve, we could expect AI to dwarf this process and undergo a rather rapid process of trial & error. Especially with the concept of connected machines and the vast availability of real-time data, we can expect the process to be fundamentally fast and unlike anything that has ever been seen before. The entire human species has used a moral compass in guiding development and uniting humanity behind a broader direction. For the first time in history, we may have a future chapter of innovation written and executed by a new kind of decision-making and at that, entirely non-human. However, we should not be blind in assuming this future is far off. As authors in Moral Decision Making Frameworks for Artificial Intelligence point out, AI is already used in highly complex ethical fields of decision making such as organ transplants and waiting lists, deciding effectively who lives a little longer and who does not. Yet one does not even have to go to medical fields to find life-altering decisions made by non-humans, where AI is already far-used in determining eligibility for receiving and underwriting credit decisions including loans, which will determine who has an opportunity to access finances for a specific reason and again, who does not. This too has far-reaching consequences. We’re already far along in introducing an objective decision maker into situations that truly matter, yet humans make a vast number of decisions each day with limited information and most importantly, limited objectivity. We shouldn’t write off the human brain however – it is truly a cognitive miracle that derives information from all senses in real time and through conscious and unconscious steering, shapes our thoughts & actions. Yet a lot of human morality centers around the concept of self-protection in complex decision making and a lot of the information accessible to humans, is a fraction of what AI will be able to tap into and process. Well Then – Can We Introduce Human Morality Into Technology? It’s certainly a possibility and one that several leading researchers and authors of our future are pursuing. For example, Future of Life Institute and Duke University have been active in the foray of introducing ethical engines into artificial intelligence and decision making by interesting applications of game theory. Researchers often look at the now-infamous examples such as the self-driving car and an unavoidable pedestrian accident and attempt to find very tangible ways of introducing intended morality in a way that is actionable and clear. It is a complex task which involves classifying actions as morally right or wrong in a universal and generally accepted way. The establishment of a pre-written ‘moral compass’ would allow an element of human decision-making to be codified and carried on into applications that will learn on their own at some point. We can generally think of the concept in different phases:

We can argue that we currently find ourselves in the first phase with the question of whether we’ll ever reach the third phase at all. Morality as a Lens for Future Outlook The future of technology and AI will likely be a series of events, some controlled and pre-planned, and others the result of unintended consequences. Morality will be a key component in determining how the future looks and the exercise of considering the absence of morality may be useful in understanding why the field’s importance is so profound. If we indeed never come to the third phase, we will also be looking at a future derived largely by a presence lacking consciousness. These elements may be impossible to imagine ahead of time, yet their implications are likely to be paramount. Written by Markus Lampinen, CEO of Crowd Valley, Inc. This post originally appeared on Let's Talk Payments.  Photo: MIT Moral Machine.

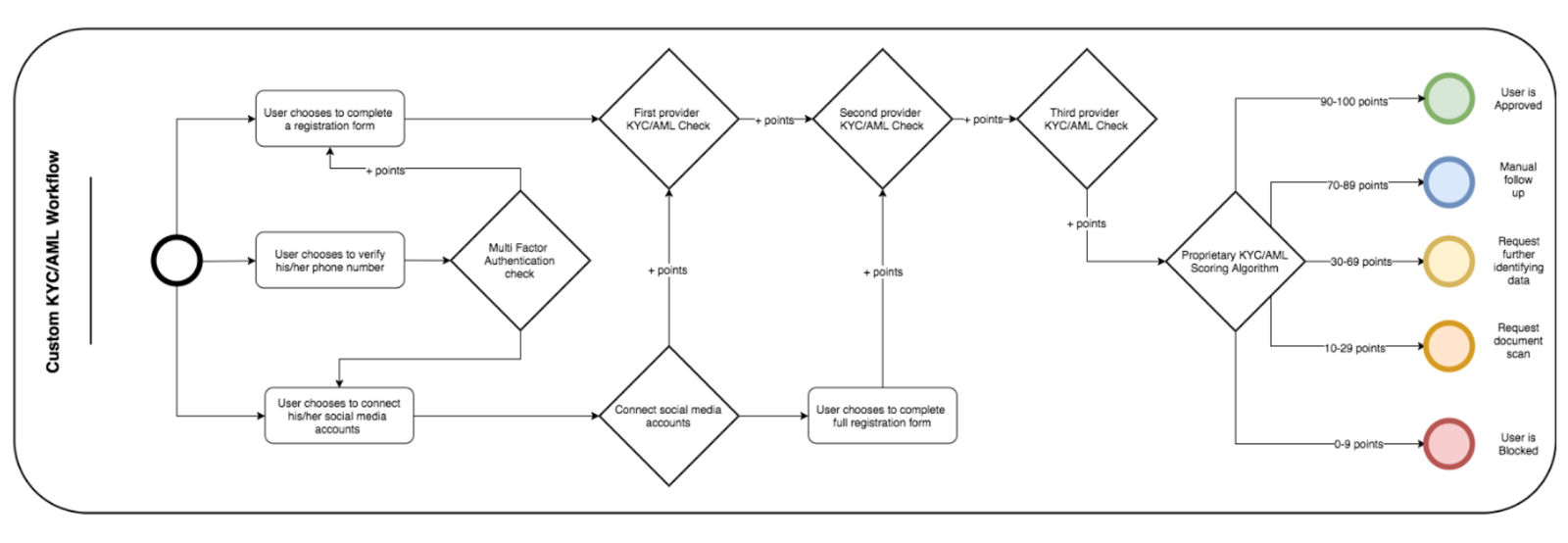

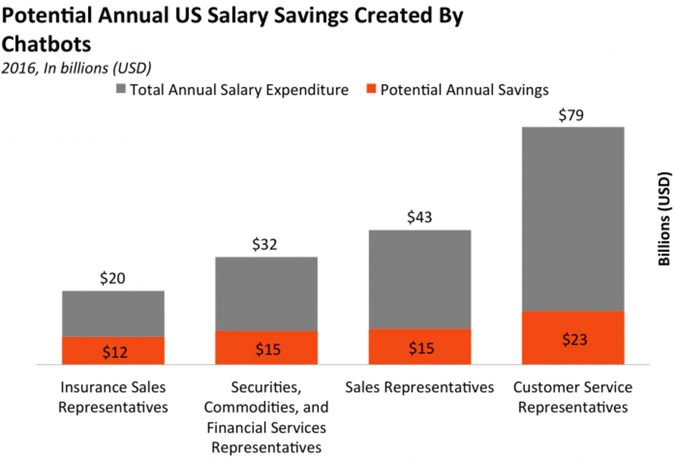

"We need new solutions for collecting and using data that strikes the right balance between consumer benefits and control over their own data." I was looking for the opening hours of a local supermarket in San Francisco from Google Maps. When I found them, Google also told me an interesting additional detail: “You visited this place 17 hours ago.” In fact, yes, I did. It reminded me that my Android phone indeed collects my every movement and location. (You can check your history at https://www.google.com/maps/timeline, when logged into your Google account.) Here’s another example of the same thing: an insurance technology (“insurtech”) company recently demonstrated its app to me, and it had a full history of drivers’ driving data, including each acceleration, braking and speeding, on the map. The insurance company collects all that data, which it can then use to try to influence driving habits, and adjust premium prices. Yet another example: new credit rating agencies that not only collect your income and loan payment history, but also try to utilize all data about you available on the Internet –including location, social network and payments – to evaluate the risk in lending you money. We are really starting to live a new type of public life, although we don’t always know it. It is not breaking news anymore that mobile, Internet services and social media collect a lot of data from us. It has been used for marketing and advertising for years. But now there are more and more ways to use it – for example, recommendations, financial services, political marketing, and personalized customer experiences. Many parties and people are very worried about this. They see that companies can now know perhaps too much about individuals, sensitive data can leak into the wrong hands, and we cannot know how the data is used in the future if ‘bad forces’ take over. That’s why governments are developing new laws and regulation for collecting, storing, processing and utilizing data – perhaps the most well-known example right now being the EU’s General Data Protection Regulation (GDPR), which takes effect in May next year. Naturally, we also hear many horror stories how this all can get worse in the future. When your phone, TV and digital assistant are listening to you speak, they can collect everything that is said in your home. Services could analyze all your communications, including emails, calls, and chat messages. There are totally new opportunities here to create intelligence gathering services much more effective than the East German Stasi ever were. And we know many government intelligence services already collect this data, or are trying to. But the flip side is the potential benefits of all this data collection. Big data analytics can make many services better. Isn’t it fair and good that your driving habits have a positive impact on your motor insurance premiums (provided you’re a good driver, of course)? Or that your life habits can determine the cost of your health and life insurance? Or your money management behaviour and spending habits can be used to evaluate the risk and price for your loan? Or services can personalize your experiences and tailor them especially for your needs and behaviors? People usually find data collection stories scary because they have no control over who gets to collect data and where and how it’s used – therefore, the simple answer is to give them control, to include the ability to forbid use of data and even to have the data deleted. In practice, of course, this is far from simple. According to different studies, the majority of people believe they had lost the control of their data. So many services collect and use data, and users are not always able to follow or control this. Companies also sell and buy data. This is a new complex area for authorities to monitor and control, although we have also seen that some Internet companies are more interested in protecting privacy and use of data than some governments. We can conclude, then, that while there are threats and risks to collecting and utilizing user data, at the same time this data is fundamental to making many services better for users, as well as more affordable. There is definitely a need for new solutions where people can manage their own data and ensure it is used to suit their needs. For example, if a person has all his or her own verified data, it would not be necessary to reveal all data for a loan application, motor insurance application or location-based service – only profile-level data that is relevant for the service in question. Today, companies are the ones collecting all the user data they can – in the future. each person should be able to collect and use their own data. At least, people should have their own copies of their data to verify that it is true. It is clear we have a need for totally new solutions to utilize data so that privacy and user control can live together. Governmental and legal control alone is not enough to handle the fundamental problems involved in data collection. (Governments can even be part of the problem of data misuse.) Instead, we will soon see a new era of data analytics that is based on fundamentals to combine personal data management, profiling and targeted utilization of profiles. The article was first published on Disruptive Asia. Check Prifina - a new way to manage your finance data.  The adoption of open APIs by banks and financial institutions has been steadily growing, as has the ecosystem delivering these services. Companies providing KYC products rank among the most well established services to help financial institutions cut cost, increase scalability and help comply in a more scrupulous regulatory environment. A Thomson Reuters global survey reveals that banks are taking as long as 48 days to onboard a new customer. Also, the banks are spending in excess of $60 million per annum on KYC and client onboarding. Although newer more dynamic platforms process KYC in an automated fashion, most financial institutions still handle KYC verifications manually. Manual verification is cumbersome and error prone. This is more true as institutions scale, adding further compliance officers compounding the problem at hand. Outside of basic requirements, Booz Allen Hamilton estimated compliance failure costing firms $13.4 billion in 2014. When taking a practical approach to deploying automated KYC workflows using open APIs into financial institutions, they need to support both technical and operation members. Technical teams are burdened with ancient core banking systems that are costly to service and as time passes, more difficult to do so. The cooperation between Fintech and financial institutions allow these technical teams to leverage cost effective solutions when compared to building and managing new infrastructure. They also vastly increase time to implement systems from an average of more than 36 months down to a period of 8 to 12 months. Making systems future proof, scalable and cost effective is a core concern being addressed by open APIs. Operational teams are focused on workflow efficiencies and the bottom line. KYC APIs allow the compliance officers to be more productive while decreasing headcount. Officers are able to monitor rather than process, needing a light touch on most onboarding workflows. Better reporting, record-keeping and the near complete reduction of manual paper work can reduce compliance failure. Decoupling the rise in deal flow with the increase of headcount allow financial institutions to scale more efficiently while mitigating compliance failure. We at Crowd Valley support both technical and operation teams migrate legacy systems into an open API environment. Technical teams can leverage our Bank grade Cloud Back Office connected to global KYC providers to efficiently launch compliance workflows into their core systems. Operational teams leverage our global reach where we have helped more than 130 institutions navigate the use of open APIs and industry best practise. If you are looking to capitalise on KYC efficiencies within the Fintech space and would like to discuss this further, please do not hesitate to get in touch with us. This post originally appeared on Crowd Valley Blog.    Fintech is growing at an astronomical rate. According to Bloomberg, more than $8 Billion has been raised in Fintech so far in 2017. Also, 5 companies have already joined the “Unicorn” status with values over $1 Billion. We have compiled a list of best Fintech reports for 2017, from some of the leading names in the industry. Fintech Reports: 1. Capgemini - The World Fintech Report 2017 Traditional Financial Services firms acknowledge the impact of Fintech on the shifting industry landscape and are confident of their innovation strategy, but they are struggling in successfully applying innovative Fintech-like capabilities to achieve tangible results. Capgemini explores some of these key issues in its World Fintech Report. 2. PwC - Global Fintech Report 2017 According to PwC, Fintech and Financial Services are competing less and coming together. PwC explores the Fintech’s growing influence on Financial Services in its Global Fintech report. 3. EY - Fintech Adoption Index EY states that Fintech has reached a tipping point.In its report, EY surveys more than 22,000 digitally active consumers which highlight the impressive and rapid growth in adoption and the variations among 20 different mature and developing markets. 4. KPMG - The Pulse of Fintech Q1 2017 | The Pulse of Fintech Q2 2017 In these reports, KPMG explores global trends and deal activity within Fintech industry including how the recent adoption of the Payment Services Directive (PSD2) is driving the Fintech activity in Europe. 5. CBInsights - Global Fintech Report Q1 2017 | Global Fintech Report Q2 2017 A comprehensive Fintech report by CBInsights which includes data-driven look at global financial technology investment trends, top deals, active investors, and corporate activity that took place in 2017. 6. Deloitte - Digital transformation in financial services Deloitte’s new study reveals that to become fully digital enterprises, many Financial Services firms may need to shift the focus inward and innovate the employee experience. 7. StartupBootcamp - The State of Fintech in 2017 This report draws out parallels seen between general technology trends on a macro scale and correlates them to the impact on Fintech. Insurtech Reports: 1. PwC - Global Insurtech Report 2017 This report is based on the responses of 189 senior Insurance Sector executives from 40 countries who participated in PwC’s Global FinTech Survey 2017. 2. Capgemini - Top Ten Trends in Insurance 2017 This report explores the two driving forces behind the insurance industry; Connected technologies and data analysis. 3. Accenture - The Rise of Insurtech A wave of startup-driven innovation is putting insurers’ approaches to innovation and technology under the spotlight, highlighting the challenges these traditional companies often face. 4. EY - Global Insurance M&A themes 2017 The increase in large deal activity could be interpreted as a sign that insurers have decided to get on with addressing their strategic priorities, despite ongoing global uncertainty. EY explores the shift in the insurance industry and adoption of Insurtech. Banking Reports: 1. Capgemini - Top Ten Trends in Banking 2017 This report aims to understand and analyze the trends in the banking industry that are expected to drive the dynamics of the banking ecosystem in the near future. 2. Accenture - Banking Technology Vision 2017 This report highlights the five trends identified in the Accenture 2017 Technology Vision that underscore the importance of focusing on “Technology for People” to achieve digital success. Payments Reports: 1. Capgemini - World Payments Report 2017 Get a preview into the Global Payments Landscape in 2017. 2. Nordea - Future of Payments Get insights from customers, partners and experts from Nordea, PwC, SWIFT, SAP and FIS. Artificial Intelligence and Blockchain Reports: 1. CoinDesk - The State of Blockchain (Q1 2017) This report includes the activities, speculations and trends in cryptocurrencies like Bitcoin, Ethereum, etc. and the Initial Coin Offering (ICO) ‘Gold rush’. 2. McKinsey - Artificial Intelligence, The Next Digital Frontier In this independent discussion paper, McKinsey experts examine the investment in artificial intelligence (AI), describe how it is being deployed by companies that have started to use these technologies across sectors, and aim to explore its potential to become a major business disrupter. This is certainly not an exhaustive list in itself, so feel free to suggest any Fintech reports, which are easily accessible, that you feel should be included above. You can also check out our post on the Top 20 Fintech Blogs to follow in 2017 and some of the Best Fintech Events and Conferences in 2017. This post originally appeared on Crowd Valley Blog.  "A decade ago we had the first big leap, and that was web to mobile,[…] Now the next one is mobile to conversational” said Edrizio de la Cruz, co-founder and CEO of Regalii, a startup whose application programming interfaces are used by dozens of financial services providers to build their chatbots. The pressure today to innovate and embrace new technology and practices is significant across a range of industries with financial services at the epicenter of the pressure but research by Econsultancy and Adobe shows that 9% of FS businesses claim to be digital first, compared to 11% across all sectors. Alongside the drive to embrace digital, there is additional pressure from the market to:

So, chatbots? Chatbots are essentially pieces of software that simulate human, natural language conversations and can respond to and act upon queries and commands from users. The advantage these systems have over a real conversation with a human is that they are able to extract and analyse a user’s needs and intent and ultimately return the information a user has requested or perform actions for them faster, at any time of day or night and at significantly lower cost than a human counterpart. The benefits of this type of technology are clear with many people choosing to apply and research investments or loans through these types of systems rather than spending the extra time and potentially cash on a human broker that may not necessarily have the best deals available. These systems could potentially pave the way to a fully automated digital process, further removing the potential for human error and bias from financial services. An apt example would be Capital One’s Eno. Eno is able to interpret text based conversational queries and commands alongside emojis. This includes the ability to check balances and pay off credit cards, while cash transfers are also in the works. Additionally for customers with Amazon Echo, Capital One has also built out a skill that allows for voice commands. At the business side, Capital One stand to make significant savings in terms of time and manpower as users transition from face-to-face and telephone queries to simply asking Eno. This is only one form that chatbots have taken on so far with the sky being the limit on the functions a chatbot might serve. Other options include:

Furthermore, chatbots do allow for a smoother digital experience overall with the ability to sync with popular applications such as Whatsapp and Facebook messenger, removing the need for an additional download that may alter existing mobile usage patterns. This interface could be instrumental in data analytics as well in improving operational efficiency, promoting innovative practices and improving the customer experience. Banks usually have a mountain of customer data at their fingertips, but often struggle to understand and get value out of it. Customer data is the key to establishing meaningful, personal relationships with banking customers and offering customized products and experiences. Banks need to effectively analyze this data to better know and serve their customers. Conversational banking enables banks to acquire more nuanced customer data. By engaging customers in small talk through conversational interfaces, banks get insight into customer intents, desires, and concerns that are not apparent in banking app and website interactions. Conversational AI can also help banks better understand this data. Through deep data analytics, pattern recognition, and predictive algorithms, chatbots can communicate intelligent insights about banking customers’ present and future banking needs. These insights can be used to offer more personalized banking products and services to build lifelong customers. There may be concern that chatbots and other AI supported technology will put significant pressure on a number of customer facing services across a range of industries due to the attractive operating margins and this is certainly true but this is analogous to the widespread worry at the time when motorized options replaced horses, a slew of new roles develop and grew out of the adoption of a new technology. An August 2016 report by Forrester suggested that banks should focus on developing the AI technology to build better bots in the future, rather than launch bots on messaging platforms now and provide poor experience to their users. The main criticism against chatbots is that they lack the empathy and the emotional response that a human can provide, which makes them less capable of dealing with complex situations involving financial decisions. Generally speaking, humans working in customer services will know how to respond to frustrated customers and not aggravate the situation; they can listen, reason, empathise and read between the lines. A lack of emotional intelligence is a serious limitation that existing bots have. There is definitely a whole new world out there to explore in considering chatbots as an investment for your own business or in a third party capacity through a promising Fintech firm but there is a degree of risk in this relatively nascent space with regards to meeting customer requirements and security. There is potential for significant secure data being shared with these interfaces as clients address their needs. In addition, Forrester (2016) found that although chatbots are developing rapidly, customer experience is not. Many fail to effectively meet users’ needs due to poor infrastructure and lack of fundamental understanding of AI. Hence it is imperative to work with institutions that have the infrastructure to support your venture effectively on the front end as well as on the back office. This post originally appeared on Crowd Valley Blog.  Source: http://www.businessinsider.com/chatbots-are-coming-to-financial-services-2016-8?IR=T

In between pauses at the WWDC, Apple announced it will be expanding their financial services strategy by going beyond Apple Pay and issuing virtual payment cards to all iOS users. There are 1bn iOS users around the world. At the same time, this same week Amazon made headlines by having lent over $1bn to third party sellers on the Amazon marketplace. Amazon has also rolled out a highly aggressive credit card offer with Chase, which offers 5 per cent cash back for its Prime customers. Neither company is a traditional financial services company. So what is going on? Due to complexity and benefits of scale, banking has historically been confined to incredibly large companies and their global operations. Sure, some are stronger in some segments or regions, but this is the broad definition of an incumbent sector. What technology has allowed over the past years is the specialization of software and therefore service providers. No longer do you have to have one stop shops for everything in finance, you can actually challenge high margin verticals, e.g. payments or foreign exchange, with a standalone business in just that market segment. Policy changes such as PSD2 play directly into this trend, setting requirements on financial institutions to open up their infrastructure in order to allow third parties access to their core processes. With globally interconnected institutions, the race into API Markets is well underway, with organizations such as BBVA, DBS, US Bank already far along. With these trends ongoing, we also find many new organizations entering finance, such as Facebook, Google and Amazon, as mentioned earlier, with a lot of personal data and connections to billions of people. It creates a perfect setting to offer a financial service, when the habits of the individual or merchant in question are known and the service, e.g. a loan can be offered at the point of the transaction in near real time. The $1bn loans issued by Amazon is a testament to this, but so too is the fact that you can send money via Facebook Messenger at the click of a button (at least in the US). Financial services are becoming increasingly embedded. The digitalization of finance is a wide-ranging theme. In addition to the companies discussed above, established banks are also modernizing their products and services, or how these products and services are offered. It seems there are two ongoing trends in different directions: 1) toward more integration of financial products in non-banks and 2) toward specialization within financial institutions. The latter may be less prominent, yet with PSD2 and pressure on margins, institutions will likely need to choose the businesses they want to invest and compete in. What is a bank? Is a bank where you place your money? Is it where your home mortgage comes from? Is it where your wealth advisor sits or who sends your payment remittance? Through specialization and an embracing of the API economy, we can expect that the future consumer will have several parties that serve their ‘banking needs’. Some of these will be companies like Amazon through the increasing position and information they hold in the market and some will be traditional banks such as Wells Fargo. Fast forward long enough, and it becomes an interesting thought experiment. Which grows in prominence, the higher margin specialized businesses or the one stop shop business that also faces the highest level of regulatory scrutiny? One thing is however certain, our concept of a “bank” is quickly becoming outdated. The bank emerged during the industrialization and has had a central role in shaping societies. Are we at a different point in history where the next paradigm shift sees information technology giants as playing a further pivotal role in shaping the societal development and if so with what implications? The “embedded bank” seems like the direction of the future. Embedded in points of interaction and specialized services, riding on the API economy and truly integrating into the customer’s life and habits, rather than serving as an interruption. How we get there is a true technological adoption across the sector over time, that places the consumer in control of their data and privacy and allows for real time decisions at the consumer’s fingertips. This post originally appeared on AltFi.  |

AboutEst. 2009 Grow VC Group is building truly global digital businesses. The focus is especially on digitization, data and fintech services. We have very hands-on approach to build businesses and we always want to make them global, scale-up and have the real entrepreneurial spirit. Download

Research Report 1/2018: Distributed Technologies - Changing Finance and the Internet Research Report 1/2017: Machines, Asia And Fintech: Rise of Globalization and Protectionism as a Consequence Fintech Hybrid Finance Whitepaper Fintech And Digital Finance Insight & Vision Whitepaper Learn More About Our Companies: Archives

January 2023

Categories |

RSS Feed

RSS Feed

|

Digital Intelligence Globally

|

© 2009-2023 Grow VC Operations Ltd. All Rights Reserved.

|