|

Grow VC Group participated in the Hong Kong FinTech events in this week. Grow VC Group Co-founder and Chairman Jouko Ahvenainen gave a keynote presentation about data and AI in FinTech, and participated in a panel discussion about future opportunities in AI and FinTech.

In the keynote presentation Jouko focused especially on the utilization of data in lending services and new models, how consumers can manage and control their own finance data. The cases are based on the work done by two Grow VC Group companies: Crowd Valley and Prifina. You can see the presentation below. The panel included the leading finance and AI gurus: Alokik Advani from Goldman Sachs, Antoine Blondeau from Sentient Technologies, Richard Vibert from Arbor Ventures, and Matthew Phillips from PwC.

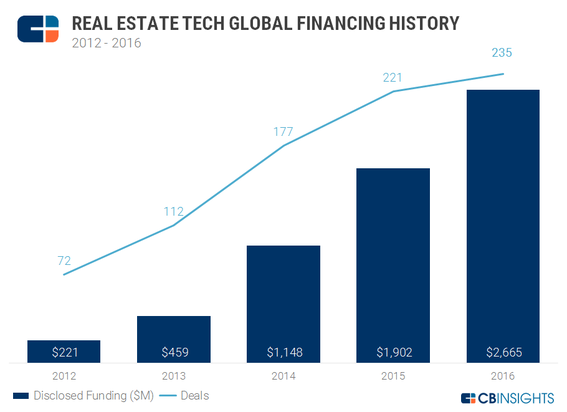

A banker recently asked me if I really believe FinTech can change the banking business. I told him, “Let’s think about a typical bank account – its user gets one salary payment, pays a few bills and handles some card transactions each month. Do you really need a billion-dollar IT system, 10,000 people and hundreds of branches to handle that nowadays?” He replied, “Now I am scared.” We can still say that a bank needs 200 persons to handle regulatory compliance and other things that are mandatory for that business, but the reality is that basic services are very simple to do with current digital technology, and a lot of layers in financial institutions are sophisticated window dressing. The fundamental problem with industry disruption for incumbent companies is that they think about services based on their existing organization, IT systems, and processes. They forget to think about what the customer actually needs. When we talk about lessons from other industries like retail and media, we hear how the finance industry still sees itself as ‘special’, and what happened elsewhere cannot happen to them. It has been said time and again in FinTech discussions that people don’t need a bank account, they need a place to keep their money and use it; they don’t need a credit card, they need credit to pay; and they don’t need investment advisors, they need help to make investments. Now with ICOs, we can probably add that people don’t need stock exchanges, they need tools to buy and trade securities. Many banks now have set up innovation or digital concept divisions that focus on developing and finding novel solutions, and working with innovative startups. Typically, however, these innovation units lead their own lives inside a bank, keeping themselves busy with their own processes and fancy events so that they have no time to actually work with startups. And operative units couldn’t care less what the innovation people do. They live inside the bank group, but are in effect on life support. I was recently in a meeting with a leading consulting firm. We talked about a new cloud-based IT solution to build finance back-office services for maybe 1/1000th of the cost of legacy systems. A senior management consultant said that this might be okay for Tier 2 or 3 banks and some newcomers, but why would the main banks change anything when they have excellent existing solutions? It’s a very similar comment that someone would have said 15 years ago why would a newspaper company use internet publishing platforms when they already have the best printing presses in the world? A few weeks ago, I had to transfer money from country A to country B. Country A uses IBAN, but country B doesn’t. So, I only had their local bank account number and the SWIFT code. But banking system in country A didn’t recognize that SWIFT code for some reason. Those codes have variations and different formats – they are not really like one standard. I could have made the transfer based only on the bank name and address, but it sounded risky. Then I found out that my bank in country C recognized the bank codes of country B, and country C had also IBAN, so I was able to transfer from country A to C by IBAN and then with other codes from C to B. I used almost two hours to set up these transfers. I also had to estimate, when the money would be in country C so I could then schedule a transfer to country B for that day. This kind of money transfer with current technology should take one minute of my time and then one second to transfer the money. Instead I spent two hours of my time and the money took four days to arrive where I wanted it to go. All the banks I used in this process were Tier 1 banks in their countries or world leading banks. I would like to have another discussion with that management consultant about whether these banks are really using state of the art technology and models and don’t need anything new. Of course, I would get many explanations – how it is not only about the technology and there are many other things that cause this user experience. I agree – there are many reasons. But now I’m talking about what the users need and want, and what can be done with the current technology. It will soon be relevant also for these leading banks when modern technology, models and users intersect. I have seen banks do new things and change their business and technology. But like all transformation projects, this requires top management contribution. The top brass must make it happen and follow its progress. Otherwise it’s left to the innovation guys hanging around at conferences, internal brainstorming sessions with no concrete action, and the operative team shooting down all new ideas – all while customers start to use digital services that actually do what they want and give them what they need. This post originally appeared on Disruptive.Asia.  The revised Payment Services Directive (PSD2) is set to change the role of banks in the financial services space. PSD2 aims to increase competition, innovation, and transparency in the EU banking sector, by opening up banking APIs to various trusted third-party services. PSD2 mandates banks and payment service providers to facilitate access to user account data and payment initiation via API, meaning that banks may no longer be the sole providers of online banking services, and instead begin acting as back-end utilities for other financial and non-financial service providers. What to expect from banks Banking APIs can be divided into five main categories: client data, account data, cards, payments, and credit. Clients Client data can act as an alternative to the various online KYC services we see today. Banking clients would be able to “login” using their personal bank details, providing the relevant third-party service with verified personal information, thereby fulfilling any KYC requirements. This allows financial and non-financial online services to piggyback on banks KYC processes, while allowing banks to monetize their KYC process outside of their own services. Accounts Account information may include bank account numbers, balances, transactions, and similar information. Accounts APIs can be used in various applications such as wealth management, robo-advising, accounting, and applications for tracking personal and/or business expenditure. Cards APIs for credit and debit cards would allow third-party services to save user's bank details without PCI compliance implications. Cards payments are of course available through various payment providers, banking APIs may however increase the competitiveness in this space. Card issuance may also become available via API, meaning that bank and credit cards can easily be issued through non-banking institutions. Payments Payments APIs mainly revolve around initiating bank transfers and retrieving the statuses of transfers. End-users could for instance sign up for subscription based services with regular bank transfers, or pay bills directly from third-party portals. Credit Credit APIs include loans and repayments. Non-banking institutions could potentially offer credit to their customers seamlessly with banks operating in the background. Furthermore, credit consolidation and aggregation could become more sophisticated with access to more data. What lies ahead? Banks may either choose to embrace PSD2 and commence building an ecosystem with their banking products in the center, while other players may take a more passive approach and comply with the regulations in the most basic manner. We expect banks with higher digital ambitions to deploy more extended APIs in order retain customer interactions and broaden access to their services in the highly competitive banking environment which is to come. Meanwhile, banks with lower digital ambitions may comply with the minimum legal API requirements, thereby holding on to their current customer base and having a lesser chance of creating a broader ecosystem. Most banking APIs are expected to roll out in the start of 2018. Banks such as BBVA have already published API documentation and started building their developer ecosystem. Other institutions such as Nordea have published a roadmap and overview of services to come. We work with leading institutions in the era of Open Banking and look forward to building out the ecosystem of available services both for the market to utilize. This post originally appeared on Crowd Valley Blog.  Big changes are happening in the financial services industry, with Fintech that has experienced a fantastic growth and with financial technology companies now on pace to see the level of investments to reach a new record in 2017. As part of this, there is a case represented by Real Estate, a trillions dollars sector that has been slow to change, which is seeing a wave of innovation with property technology, or Proptech.  We talked about Real Estate crowdfunding different times already, but when speaking about Proptech, we are considering a far broader segment, referring more in general to those companies using technology to “improve or reinvent the services we rely on in the property industry to buy, rent, sell, build, heat or manage residential and commercial property”, improving a range of related services from the access to mortgages to building energy efficient homes. And we are now starting to have very concrete examples about how this is changing the property market. An illiquid market where it’s expensive to trade property and where “there is a large risk of abortive expenditure, and the result can be a very wide bid-offer spread” is listed as one of the key Real Estate’s current limit in a report called “PropTech 3.0: the future of real estate”, recently published by Professor Andrew Baum of the Saïd Business School at the University of Oxford. “Crowdfunding platforms, on line secondary market platforms and blockchain make this the most intriguing of FinTech questions. It seems very likely that the many tech-based contributions to the residential sales process will bear fruit. If investor protection issues can be solved, tech platforms will enable smaller residential assets to transact on platforms and exchanges in reasonable quantity, leading to exponential growth and radical change.” said Professor Baum. Alex Gosling, CEO of HouseSimple.com, says that he managed the sale of more than 18,000 properties since the launch of its platform in 2015, with a rough £40M (approximately $54M) saved, considering the usual agent fee charged on the average UK house price. “As more people feel comfortable with the online model, we expect online agents to grab a bigger slice of the UK estate agency market. Currently, online estate agents have around 5% market share. We believe this will increase to 15%–20% by 2020,” Gosling says. Returning to an area more familiar to our readers, there is RealtyShares, a San Francisco based company that just raised a new funding round of $28M, led by Cross Creek Advisors. They developed a debt and equity Real Estate investments platform, that since its launch in 2013, has deployed $500M across more than 1,000 properties, with a typical transaction size between $2M and $5M. Another good example of Proptech company that is doing well is Habito, a digital mortgage broker that just received investments for £18.5M (approximately $25M), in a raise led by the venture capital fund Atomico. Since its launch in April last year, Habito advised over 50,000 people on mortgages worth more than half a billion pounds. Niall Wass, Partner at Atomico, said that the big inefficiencies within the mortgage market present at the moment an attractive investment opportunity. Looking more in general at the market, Proptech companies received about $6.4B in investments across 817 deals since 2012, with investments from venture capital that peaked last year. In 2017, with $1.46B already invested across 107 deals in the first part of the year, the total amount of dollars invested is expected to reach $3.4B, exceeding 2016 by 25%. We will need to wait to see how the market will develop in the future, but the perspectives at the moment certainly seem very positive, not the least considering the massive scale of the labor intense global property market. This post originally appeared on Crowd Valley Blog.  Source: CB Insights - https://www.cbinsights.com/research/real-estate-tech-startup-funding/

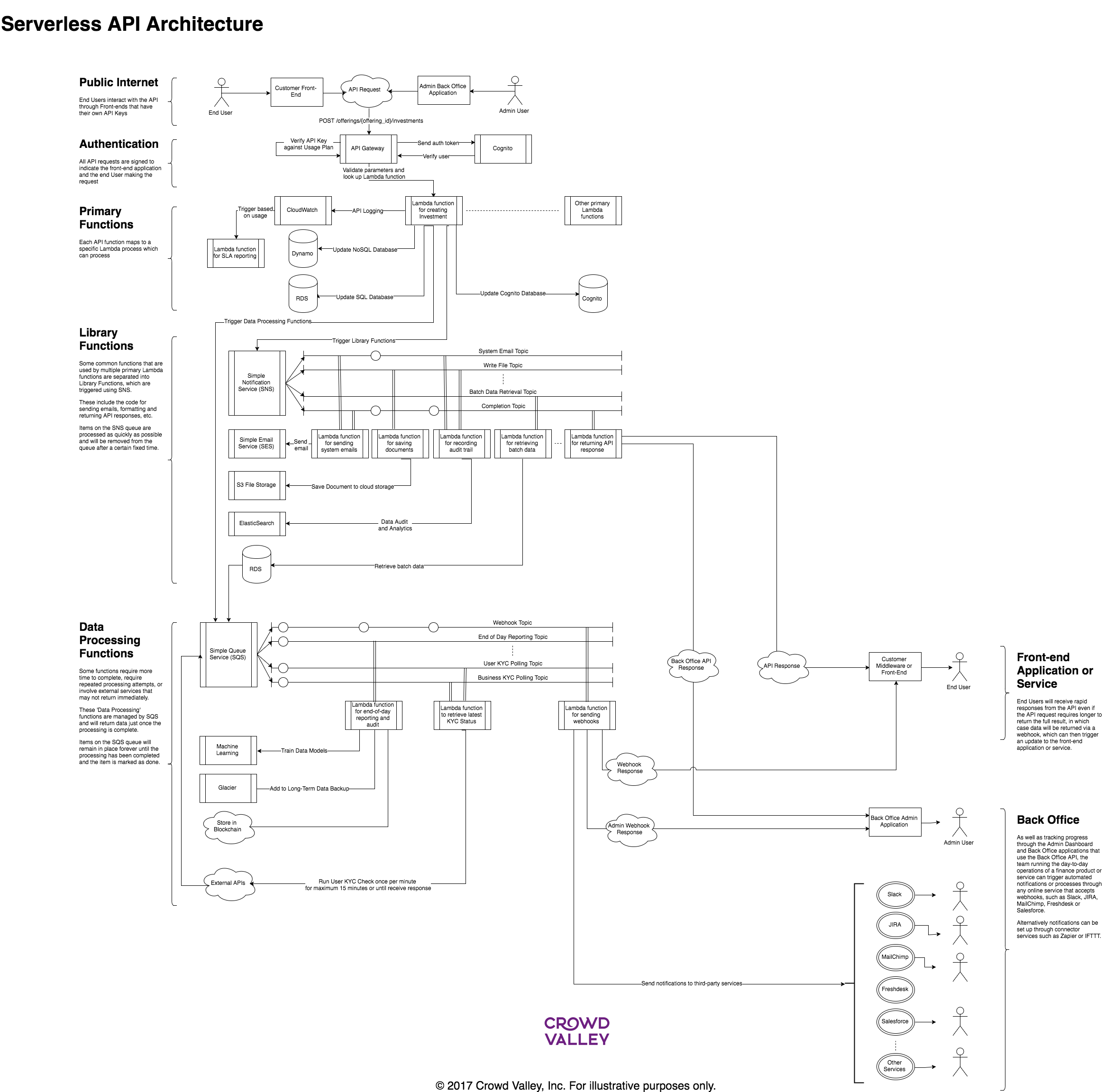

With the Payment Services Directive becoming a reality at the start of 2018, can we expect to see a panacea of connected services at users’ fingertips, offering best in class quotes for financial products based on actual information? Will we see firms position themselves as leaders beyond their previous borders and existence, in the digital realm with limitless data-driven possibilities? Or will we maybe see cross the board resistance and siloed architecture that prevents valuable use? If you are looking for the short answer, here it is: Yes. If on the other hand you can accept the reality will be multidimensional and layered, well the answer is still “Yes”. In any new market, and let’s be very clear this is a new market, we will see behavior and approaches from each end of the spectrum searching for their preferred way to adapt and benefit from the new reality. With the inception of financial digitalization, we’ve seen new firms such as Goldman Sachs adapt their strategy to cover retail and embrace fintech, firms such as Citi and BNY Mellon have ventured into open banking and finance APIs and Vanguard has created a digital behemoth of their robo-advisor. Yet for each firm there are dozens that are still in 2017 evaluating their position and strategy, laying out plans that have yet to see the public and some still on the fence. Having started looking at the market in 2009, it was clear the market would not move in uniform fashion yet the complexity of the market and its adoption of new technologies and paradigms was still a surprise. Open Banking is still a new concept and, as new concepts go, it will be refined by trial and error. Some banks are farther along than others, with e.g. BBVA already in commercial use with several APIs. Yet the roll out of new “API Markets”, as they are often called, will see a learning experience from both the bank providers as well as those looking to utilize them. From our experience working alongside many of these Open Banking interfaces, there are areas that require more than just a technical understanding, such as client on-boarding and related requirements around KYC and AML, not just the requirements but how institutions like global banks actually deal with them; these impact behavior, use and ultimately the design of new products and services. We’ve talked about opportunities with PSD2 before, including the Open Banking concept of how a full financial app ecosystem will emerge on top of the Open Banking platform with extensive business implications. One thing we are beginning to see is how the concept of Open Banking can fundamentally shape and transform mandates, where financial institutions may see their services and opportunities broaden beyond their traditional operations. And how would this happen? For one, it may happen organically by the very virtue of having an open platform and allowing the third party ecosystem to truly flourish. Banks may indeed find new customers that they did not consider previously, from places they are not active in – whether that be a geographical area or a market segment. Whatever we foresee with PSD2 and Open Banking, we are likely going to be right. It’s going to be a direction we follow and a little bit of everything along the way. Yet as an industry as long as we are focused on ultimate client value, that direction should guide us along. Written by Markus Lampinen, Crowd Valley CEO This post originally appeared on AltFi.  Clouds have become the standard for many online services. Now we are really moving to serverless services that offer many benefits over the traditional cloud server models. Serverless architecture can offer better use of resources, more cost-effective pricing and also better security against some threats. There are, of course, still servers in serverless solutions. Serverless means dynamic allocation of server resources, i.e. we don’t need to pay or rent dedicated servers, but we buy computing capacity and we can use it based on our needs. These solutions are also called Function-as-a-Service, FaaS. Most leading cloud providers already offer serveless services, for example, AWS Lambda, Google Cloud Functions, IBM OpenWhisk, and Microsoft Azure Functions. Serverless models also change software architecture. The microservices model means that each small task or job is a separate function that works independently. For example, in a finance service a KYC process (know-your-customer) can have an independent ID check, sanction list and anti-money laundering checks, so that all of them are independent functions that can run in parallel too (see an implementation example in the picture). This model enables the development of more independent functions by different developers and also makes it easier to debug smaller functions - and the same functionality can be then used for different services. Of course, starting and running many functions also creates some overhead, but it is quite small compared to the benefits. This doesn’t mean that all services need to become microservices, it is possible to also create functions that handle bigger tasks. Serverless means that a service provider needs to pay only for the capacity actually used. This is especially valuable for services where capacity needs vary. Earlier a service needed capacity based on peak demand, but with serverless models the service pays for the functions executed in the cloud service. These solutions neither take resources for traditional server setup or management work. The concept also makes it easier to implement API services that can process in the background and an API call doesn’t lock any other services. For example, a user can ask his / her investment portfolio details. The back office API replies immediately that it will be processed. The actual data then comes in several patches through webhooks to the front end. This can help also with blockchain implementations, when blockchain functions often don’t guarantee any latency time. The serverless model works very well for many digital services, but of course, there are still some services where the traditional server model is faster and more cost-effective. For example, services that constantly require a lot of computing capacity are probably better to run in the traditional environment to avoid the overhead required to constantly start tasks when capacity is needed. When the load is easy to predict, it is also cost-effective to rent an optimal server capacity. Most internet and mobile services have off-peak and on-peak periods. FinTech services are one example of those. If we think for example about payments, finance back office functions, and banking services, load needs vary a lot. They are also often critical services, i.e. they must work properly also during a peak demand. Serverless solutions can also offer better security against some threats. For example, a serverless solution is more immune against denial of service (DoS) attacks, when the service is not dependent on certain servers. An attack can create additional costs, if it means a lot of capacity is used for in-coming requests, and attackers with massive capacity can target a whole cloud. Some serverless clouds (at least AWS Lambda) offer tools to require API key or authentication for a function. This means a DoS creates only API calls to the API gateway, but don’t start more processing - this eliminates the load and cost effects of DoS. The model also helps against attacks that compromise individual servers that are then used to attack further. Serverless also eliminates problems caused by unpatched server software. This doesn’t mean all of this comes without any potential issues and security risks. Vulnerabilities in software and applications are still a risk. Serverless can also make traditional security monitoring more complex. As a whole we can conclude that serverless can help with security risks, but it also needs competence to manage vulnerabilities and a new kind of software and data architecture. FinTech is a fast-growing service area that is also moving to clouds. This is a good timing also consider serverless solutions for finance applications, especially when they can also help with security. You can already develop a serverless payment solutions with Stripe. Crowd Valley is piloting serverless version of its finance back office as a service. US bank Capital One has been reported to be an AWS Lambda customer. Thomson Reuters and US finance industry self-regulator Finra also already use serverless solutions. Serverless solutions will most probably come to dominate all event-based services. It fits well to financial services too, and timing with many other new things in finance is now good to make the transition. For example, the PSD2 regulation will open APIs to banking services and will significantly change finance services and their structures (read about old banking APIs). Serverless can offer a lot of value to create more cost effective and stable services, but of course they also need their own competencies to do it right. This post originally appeared on Telecom Asia.  |

AboutEst. 2009 Grow VC Group is building truly global digital businesses. The focus is especially on digitization, data and fintech services. We have very hands-on approach to build businesses and we always want to make them global, scale-up and have the real entrepreneurial spirit. Download

Research Report 1/2018: Distributed Technologies - Changing Finance and the Internet Research Report 1/2017: Machines, Asia And Fintech: Rise of Globalization and Protectionism as a Consequence Fintech Hybrid Finance Whitepaper Fintech And Digital Finance Insight & Vision Whitepaper Learn More About Our Companies: Archives

January 2023

Categories |

RSS Feed

RSS Feed

|

Digital Intelligence Globally

|

© 2009-2023 Grow VC Operations Ltd. All Rights Reserved.

|