|

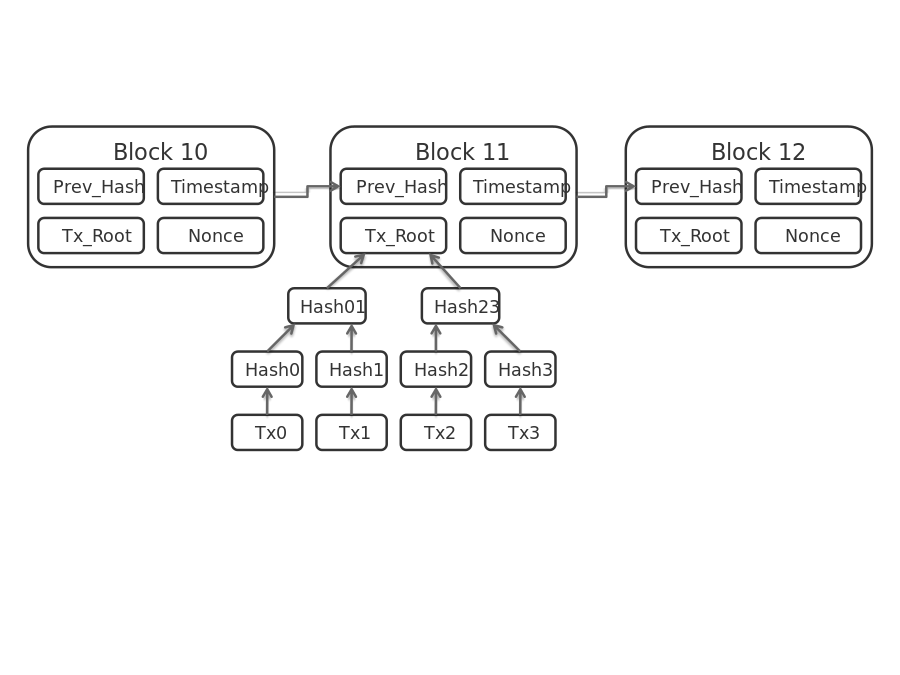

There’s a lot of excitement about blockchain and the opportunities it offers the financial services ecosystem, but a lot of work is still needed on bridging the learning curve around actual applications and implications. The very fabric of blockchain, it is distributed, is what makes it both interesting and at the same time, difficult to fit into current structures. Blockchain is technology that lets people ‘sign contracts’ electronically — without the requirement of a trusted third party (such as a government or a lawyer or a bank) to verify the contract as valid and legal. "Signing a contract" could be interpreted pretty broadly. For instance it could mean performing a trade of shares, transferring Bitcoin between accounts, Signing a will, purchasing a coke from a vendor machine, moving a train ticket to your phone and being able to prove you have it or essentially any interaction between people or entities, regardless of industry or action. In the blockchain, every time a transaction occurs, a block of data is added to a digital chain. For example, if person (A) transfers money or information to person (B) this transaction will be logged in the blockchain with a certain code. The blockchain creates trust because a complete copy of the chain, which shows every transaction, is held by the entire network. If someone attempts to cheat the system or steal, they can be easily identified. The concept of distributed presented by blockchain is inherently difficult to grasp. The fact that an online application is distributed between a network of machines, powers technical redundancy and works in its own right to protect the entire system, i.e. the blockchain. However, fitting this into current mandates around central control and governance in the stakeholder ecosystem is complex to say the least. Policy is created on the basis of governance and special access, if needed, to ensure that policy enforcers (for example regulators) can fulfill their own capacity and function. The blockchain offers an unencumbered transparency previously impossible, and a comparable ledgering of transactions to that of the exchange traded assets on public markets. The concept of having a universal timeline of sorts, to companies, transactions and even individuals is an interesting thought process, allowing to trace transactions back to their origin and find the entire value chain that led to a certain transaction. There are clever ways of attempting to harness the positive and mitigate the risks, for example with sophisticated access rights and different layers of information accessible by different stakeholders, yet the ultimate transaction remaining public record. Read the whole article on Crowd Valley News. Photo: blockchain data transaction model (Wikipedia).  |

AboutEst. 2009 Grow VC Group is building truly global digital businesses. The focus is especially on digitization, data and fintech services. We have very hands-on approach to build businesses and we always want to make them global, scale-up and have the real entrepreneurial spirit. Download

Research Report 1/2018: Distributed Technologies - Changing Finance and the Internet Research Report 1/2017: Machines, Asia And Fintech: Rise of Globalization and Protectionism as a Consequence Fintech Hybrid Finance Whitepaper Fintech And Digital Finance Insight & Vision Whitepaper Learn More About Our Companies: Archives

January 2023

Categories |

RSS Feed

RSS Feed

|

Digital Intelligence Globally

|

© 2009-2023 Grow VC Operations Ltd. All Rights Reserved.

|