|

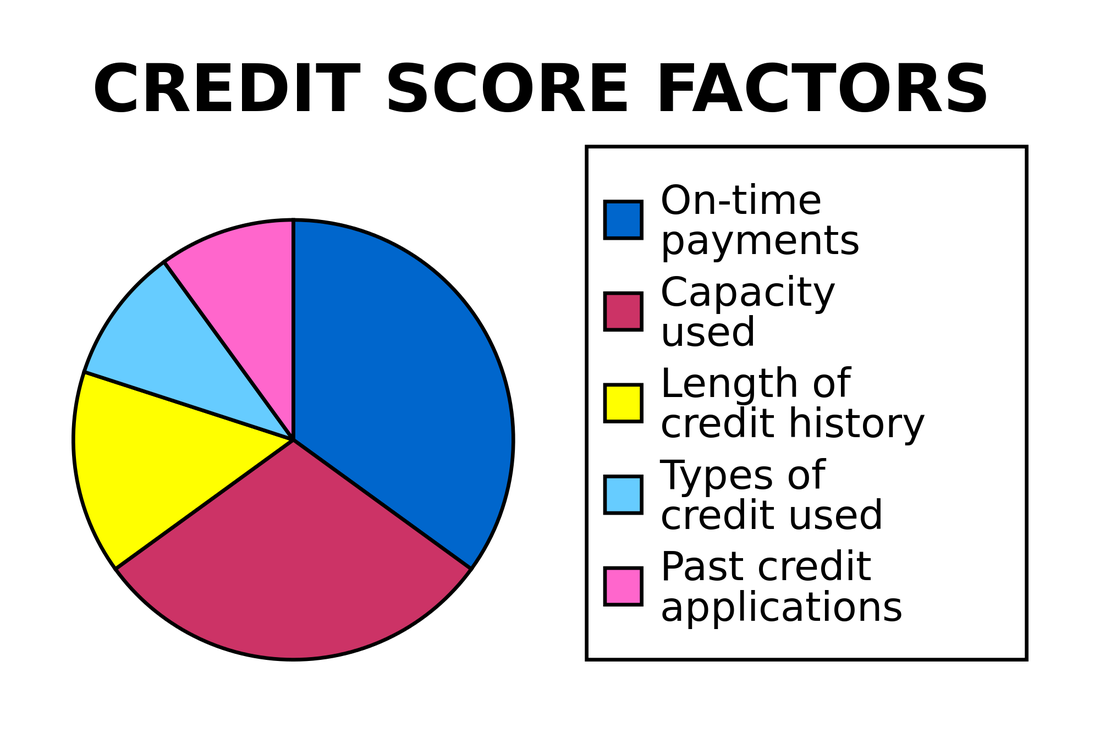

Over two billion working-age people have no access to ordinary finance services, like bank accounts, payment cards or loans. These people are especially in developing countries and emerging economies. But not only there, for example, in the UK two million people cannot open a bank account. Finance services are key for many other things in life, without them people are outsiders. Fintech and mobile can change all of this. People don’t need a credit card, they need credit. People don’t need a bank account, they need a safe place to keep their money, an easy way to receive money and make payments. When we think about solutions for financial inclusion, it is not about a focus on old finance services, but how to utilize technology and directly embrace the next generation solutions. Financial inclusion is not only about tools to handle money. Financial data is a very important part of inclusion. Know-your-customer (KYC), credit ratings, and finance history are crucial elements in most of finance services. Without financial data a person is not able to benefit from most of financial services. Many companies are now developing services that enable excluded people to receive their salary into an online account, make payments, transfer money to the family, and even apply for loans. Those solutions definitely help these people. It helps also economies, when for example the solutions can help collect tax information and pay taxes. But they are only the first steps. Especially finance data and creditworthiness needs further solutions. It is also important that people are not tied to one service alone and its own customer history, but people are able to use different services, compare them and prove their history there too. Traditional credit rating is missing or inadequate in many developing countries. At the same time we see many problems in credit ratings in the most developed countries too. It can be problematic especially for young people and immigrants, who start from scratch. At the same time there are privacy concerns. Circumstances of people nowadays can change rapidly, when there are societal changes in working relationships and even family relationships compared to earlier. All this means we need new solutions for financial data and ‘finance-ability’. The need exists in the developing and developed countries. Actually, it is not only for people, but SMEs too. SMEs encounter the same problem, and sometimes it’s even worse. It is difficult to open a bank account with all regulatory requirements for banks, and acquiring debt capital for an SME is particularly cumbersome. We need totally new angles to solve this problem. The relevant data is not necessarily only data from finance services, but many other data points to help address requirements around knowing the customer and also considering his or her creditworthiness. This is a significant opportunity for fintech companies, but also for other parties, for example, mobile carriers can have a role in this. Most probably it doesn’t make sense for carriers themselves to enter the finance data business, but opportunities for partnerships are emerging in these services. Financial inclusion is one of the biggest fintech business opportunities. But it is not only a business opportunity; it enables a normal life and equal opportunities for now excluded people. It is also important for countries and economies, when all residents are included properly in the economy and also pay taxes. Financial data and finance-ability is an important part of this and it requires cooperation of many parties that offer data and develop data solutions. In practice, it means, for example, cooperation of fintech companies, mobile carriers, retail companies and governments. This article was first published on Telecom Asia. Prifina (a Grow VC Group company) develops new solutions for financial inclusion data management.  |

AboutEst. 2009 Grow VC Group is building truly global digital businesses. The focus is especially on digitization, data and fintech services. We have very hands-on approach to build businesses and we always want to make them global, scale-up and have the real entrepreneurial spirit. Download

Research Report 1/2018: Distributed Technologies - Changing Finance and the Internet Research Report 1/2017: Machines, Asia And Fintech: Rise of Globalization and Protectionism as a Consequence Fintech Hybrid Finance Whitepaper Fintech And Digital Finance Insight & Vision Whitepaper Learn More About Our Companies: Archives

January 2023

Categories |

RSS Feed

RSS Feed

|

Digital Intelligence Globally

|

© 2009-2023 Grow VC Operations Ltd. All Rights Reserved.

|