|

In the EU banks must open APIs to their services, and banks plan these steps also outside the EU. Some see it as a threat and some as an opportunity for banks. But one question is whether this is so relevant anymore. Some years ago, telcos started to talk about telco 2.0 and open telco APIs, but they haven’t really become anything significant. Can it be the same situation for banking APIs? Telcos have wanted to open APIs for many years and in that way, for example, enable third parties to offer communications services that are based on telco infrastructure. This never took off, but they have also tried to revise the concept and activate it again. There are probably a lot of reasons for this failure, for example:

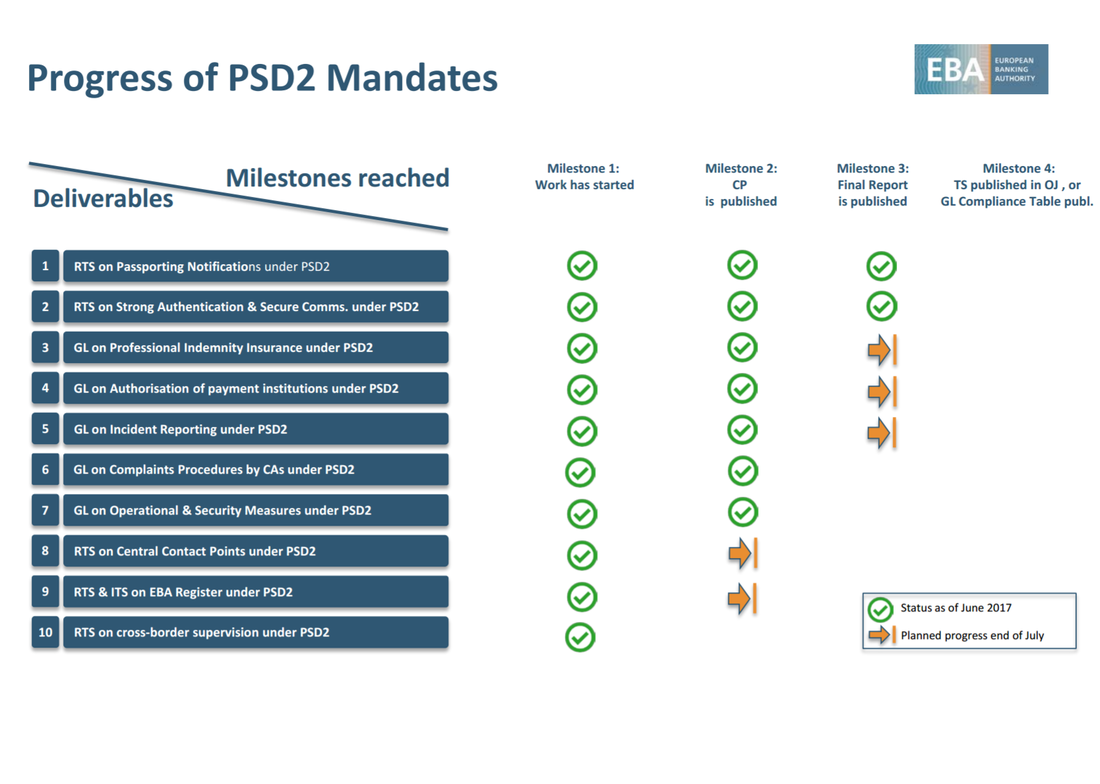

Banking API requirements are coming especially from EU’s PSD2 directive that targets to open opportunities for third parties to offer payment, accounts and finance data services by utilizing banking infrastructure and regulated banking services. It is basically intended to increase competition within finance services. At the same time, several banks have seen it as a business opportunity offer open APIs to their services and infrastructure. We can easily see that there are quite a lot of similarities between telcos and banks in terms of open API business. The question is then, if banks can do it better than telcos have done. Or is it actually the case that those old-world services and APIs are not the way to build any truly novel services? It is important to remember that the open API business needs much more than open technology APIs. An open API is relevant only if another party sees it is the best way to implement a certain service. To achieve that it requires at least four things:

There have been speculation and rumors as to how some banks might want to make it intentionally difficult to use these services, and in this way, they can limit competition. We have seen similar things in the telco industry, when the telcos needed to offer capacity, facilities and number portability to other service providers. I have also personally seen that in the telco industry it was not enough that a telco and its management were committed to offer these services, but many lower level employees were not willing to really get them to work. They still felt it difficult to offer something to potential competitors, or they didn’t like that the business changed and required new things from them too. So, this is in many ways also a matter of the organization culture. Considering all the points above, we can see the open APIs to banking services is not such an easy thing to work in practice. The question is especially if those APIs offer a really competitive and trusted way to implement services. Legacy banking IT infrastructure is quite old, it is complex and expensive to make any modifications to it, banks have no technology or business competence for open API business, there are constant new modern technology solutions to implement similar things, and new service providers might have problems in trusting banks so that they really would be dependent on them. At the same time, other alternatives like cloud based finance back offices, payment gateways and distributed ledger type solutions are emerging and might offer more competitive ways to build services. The ultimate question is if banks really want to get the open API business to work. If they want, they must really consider all aspects of the business and technology. It might require fundamental changes for their competence, technology and culture. They must realize that they won’t be the gate keepers to many of these services in the future. They must offer a real competitive solution and value. This article was first published on Telecom Asia.  |

AboutEst. 2009 Grow VC Group is building truly global digital businesses. The focus is especially on digitization, data and fintech services. We have very hands-on approach to build businesses and we always want to make them global, scale-up and have the real entrepreneurial spirit. Download

Research Report 1/2018: Distributed Technologies - Changing Finance and the Internet Research Report 1/2017: Machines, Asia And Fintech: Rise of Globalization and Protectionism as a Consequence Fintech Hybrid Finance Whitepaper Fintech And Digital Finance Insight & Vision Whitepaper Learn More About Our Companies: Archives

January 2023

Categories |

RSS Feed

RSS Feed

|

Digital Intelligence Globally

|

© 2009-2023 Grow VC Operations Ltd. All Rights Reserved.

|