|

Fake news has been a popular topic for a few years, especially how it impacts politics and elections. Fake videos are becoming more relevant too, especially when technology enables the creation of videos where faces and voices can be seamlessly implanted. The most recent Mark Zuckerberg fake video was a reminder that this is really happening. However, a potentially more dangerous threat comes from fake data in all formats and why it is also a bigger personal risk than data leakages. The idea of fake news, videos or data more generally is to have something that people believe to be authentic or valid, even though it is not. The fake material is then used to change people’s opinion, sway decisions or cast a slur on someone. They are used frequently in politics but can also be used in business, for example, to cause trouble for a company, manipulate stock prices or create support for competitive businesses or companies. At both business and personal levels, stolen data and misuse of confidential data have been the main issues, e.g. someone uses a company’s business secrets, steals an identity, or reveals personally sensitive information. As we know, this can cause all kind of business and personal issues, but it is not always the worst option – what if data was fake? Someone can create fake rumors about a person, or a company and they are a kind of fake news. Fake rumors are probably a very old model to cause harm to someone and it is very hard to fight against them, if they are good stories. How about going deeper into your data. What if someone could create a new credit history for you, new family details, a criminal record or health records. Basically, many parties have a lot of data about us and it has a lot of impact on our lives, but if that data was modified, it could really cause trouble. Let’s imagine a storyline for a thriller where a person’s entire historical information is changed. He doesn’t work in his workplace anymore, he doesn’t live in his house, he isn’t married to his partner, isn’t the parent of his children, doesn’t have access to his bank account and isn’t the person in his passport. Basically, the person would longer be the person in his or her life. The scary part is that this is no longer a fictional plot for a TV series – it could actually happen to someone. You might say this fake data was easier to create before the digital era with paper documents. While it may be true, with digital information the impact of fake data can be much greater, and it can be generated at a much larger scale. The fake data can be distributed to many places quickly. There are already examples, how a simple error in one master system changed the name of a person, the new name is distributed to all relevant places, including the passport office, health care service and banks. Suddenly the person cannot use any services with his real name and his ID is no longer valid. If your fingerprints and face don’t match the government’s passport and ID database, which is considered to be the real one? Fighting against fake data needs other means than just protection of data from leaks and theft. We can say there should be enough safe places where the information is hard enough to change. There should also be models on how to handle information that seems to be incorrect. In practice, this requires complex models, with no system totally safe it is hard to know what information is really correct, or if some information has been modified. This requires planning on how to handle this risk. Some organizations and people might still say it is enough to have safe authority, bank and health care organization databases that have the master copies of the data, but this is naïve thinking. We have seen enough cases that prove no system is totally safe. An important aspect is also the legal protection of individuals. If your digital data is only stored and managed by the government, banks, health care organizations and big companies, how can you prove that your data is correct or even know if it is correct in those systems. Individuals should be able to protect against criminals but also against government, authorities and big businesses. But how do you do it if they manage all your data? We are starting to see possible solutions to prevent this threat. For example, solutions to control personal data, blockchain type solutions to track all transactions and history of changes and models to check data from reliable sources and verify its integrity. But we are still in the very early stages. The first step is really to recognize the risk and include it in the design and regulation of data systems. Data already plays a central role to drive our daily life. We must be able to guarantee that our data is correct, and that it is me who defines my data and not that the data makes me someone else. The article first appeared at Disruptive.Asia. Read more about new data models and virtual assistant at Prifina.  Data has been referred as the oil, blood vessel or cornerstone of business nowadays. But it is a very unequally distributed asset. Some giants, like Facebook, Google and Amazon, have much more than others. Once upon a time the Rockefeller oil company was split under the antirust act. Should the regulators do the same to data giants, or can the market handle them? We have many big companies around the world, like telco carriers, retail chains, TV and publishing companies and banks. They have millions of customers in their home and foreign markets. What do they all have in common? They want to utilize customer data in their operations. But suddenly they have found themselves in a situation, where they cannot compete in data with the Internet giants. Even the biggest publishing companies do not have better or even enough data to compete with Facebook to target advertising. Retail chains cannot compete in data with Amazon. There are also rumors that if these companies were to launch finance services, banks would have a tough time to compete with them. Telcos basically were the source of data, but nowadays Google and Facebook know their customers better. This situation has especially led the EU to investigate these companies and how they utilize their strong positions in the market. There are, at least, speculations, how Facebook, Google (Alphabet) and Amazon could be split. Amazon’s position, in particular, has created political pressure in the US, when many retailers are in big trouble. Although we often hear speculation about antitrust laws especially in the US and the EU, it is not so typical to split companies. It is often also said that technology and markets are changing so rapidly today that it is not necessary to split companies anymore. The market will take care of them. A typical example in this context is Microsoft. In the late 1990’s it dominated the PC operating system and software markets. But mobile, Internet and cloud services have changed the market and no one sees Microsoft as dominating the market anymore. If we think data, is it realistic to think, the market could handle this. There are companies that are data aggregators, collect data from many sources and sell it. In that way companies can buy more data. But probably this is not enough to compete with those that are really in touch (or in the mobiles) of each individual. And privacy requirements have even more impact on data trading than on collecting it. So, could anyone have more data on you than Facebook, Google or Amazon? There is one party that has even more of your data. But the question is, if this party can really operate on the data market and change the market and competition situation. Or if this party technically can really make it easy to control and use the data? Who is this party that knows more about you and collects more of your data? Government, bank or your local Internet provider? No, it is you, yourself. You can still know more about yourself than any Internet company and also collect more of your own data. But you would need better tools to do it and to really control your data. If you can carry your data or purchasing profile to your supermarket, or use your profile to select the best offers for you or to have your financial profile to find loans and wealth management products for you, it would be impossible for Google, Facebook or Amazon to compete with your data. It would be a real disruption for the data market. Data defines your life and what you can get nowadays. It is a threat that a few gigantic companies in the world control your data. It doesn’t stop with these companies, if governments start to collect all these data points and force companies to hand them over, it can mean many new risks. Data doesn’t only impact your human rights, but it starts to be your human right. If the solution for data control is not to split some companies and hope to have governments that respect human rights, but to enable people to own and control their own data. Then it would change the whole data business, how centralized Internet has worked and how people can control their own data. The good news is that distributed data models, blockchain and the changing urgency and discussion about privacy are going to enable this soon. Once the Internet was expected to make the world more open and equal. It has happened in some areas, but data and some services has become very centralized. Now we see signs, that we can go to more distributed models, where human beings can control their own roles and even get a personal AI to help them. The article first appeared at Disruptive.Asia. Read more about personal data and virtual assistant at Prifina.

AI and robots are going to take work from human beings, there is no question about it. The much more complex question, as usual, with new technology, is how exactly it will happen and what is the timetable. We know robots have already taken over some factory work and self-driving cars are coming, but robots are also coming to the office and information work, for example, at JP Morgan, software takes standard legal work from lawyers. But maybe Robot Processing Automation (RPA) and outsourcing office robots is the next big wave to start some real disruption.

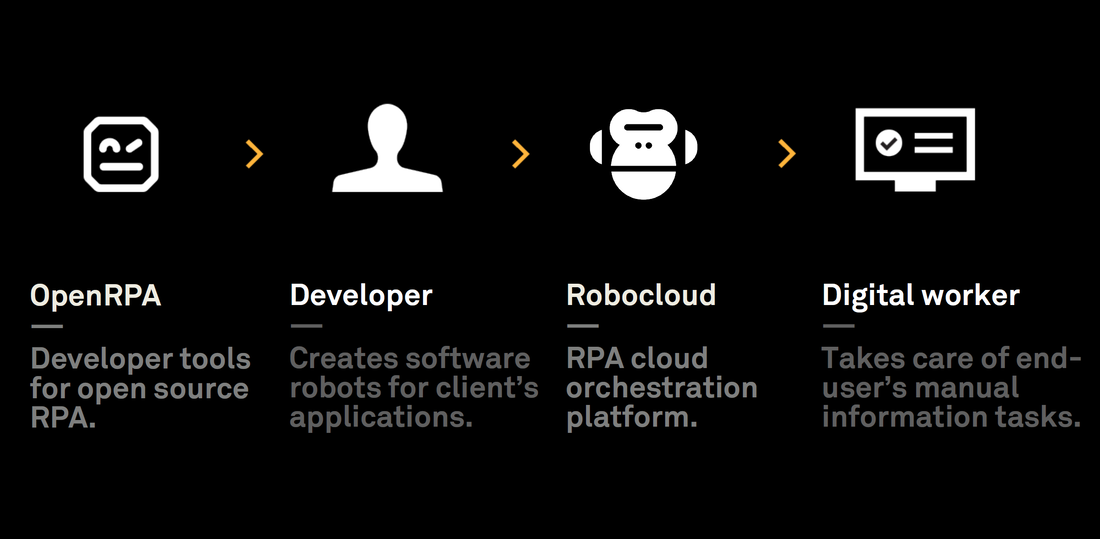

RPA is already a two-billion-dollar plus global market and is expected to double in three years. RPA is the technology that allows us to build computer software (“robot”) to emulate the actions of a human interacting with computer systems. RPA robots utilize the user interface to capture data and manipulate applications just like humans do. Basically, it means software uses systems as a human being and can also process data between systems. In practice, it can be simple data transfer from legacy systems to some new system, or from Excel to SAP, but it can be also handle much more complex processes such as insurance claims. At the moment the RPA market is dominated by a few big software companies and system integrators that manage implementations. To get to the next level, it needs lower license fees for robots, but also making the actual implementation easier. Easier implementation doesn’t mean only easier tools to make simple tasks, but also more powerful tools to make much more advanced robots that can handle much more demanding jobs, even including AI. A potential business model is to start to offer outsourcing services done by software robots. Business Process Outsourcing market is expected to be a $343 billion market by 2025. We can say it is almost 100 times the current RPA market. Nowadays RPA is mainly used in larger corporations that want to cut routine work. They make their internal calculations; how much human work must be replaced that they have a business case. Then they approach a larger IT consulting or System Integrator firms and buy an implementation project from them on RPA software. Then they pay license fees to RPA software vendors. The license fees are quite high, so it must be significant savings in the human work that this implementation project and software fees are really justified. At the same time some companies have hundreds of other tasks that could be automated. And there are also thousands or hundreds of thousands of smaller companies that also must perform a lot of routine work. Let’s think, for example, smaller accounting firms. Their employees use a lot of time copy-pasting information between invoicing, payroll, reporting and accounting systems. Sometimes they build some of their own ‘macros’, but in the most cases it is too complex and they have no time to optimize existing systems and processes. They probably can’t really justify a business case to use the current RPA software solutions. Let’s then think, if they could easily take a cloud-based robot that starts to handle routine tasks between an invoicing and accounting system. A small company could order a robot online for its specific needs and we had cloud-based solutions where hundreds of thousands of developers could develop and offer their robots to companies of any size. It would be easy and safe to start to use those robots for daily office routines. This would really change the office work and the role of robots in information work. Then it would be easy to build more complex functionality, including AI, into those robots and to get them to execute more and more complex tasks. We are already seeing all kinds of physical robots. There are industrial robots for manufacturing, waste-processing and transporting items. We also have cleaning robots in homes and self-driving cars. It’s somehow surprising that software robots for office work are still so complex to build and so expensive. It is clear, however, that this is going to change. Today the RPA market is like any boring B2B software market. As we know, big changes are not really implemented by selling software in a traditional way to companies, especially when the targets are mainly larger companies that are conservative, procurement channels are ultra-conservative and both are influenced by opportunistic IT consulting firms. It is very evident that software robots will, at some point, be found each and every office. The question is now, how and when it will happen. A strong candidate is to have platforms that easily build and enable robots and offer them for outsourcing work. When it starts to happen in a big way, no office will stay the same. Maybe this is one new area where Silicon Valley and China could start to put money to work? The article first appeared on Disruptive.Asia. Read more about Robocorp, the leading cloud-based open source software robotics company. Prifina has been taken position 21 on AngelList's 32 Fastest Growing Startups In San Francisco - Hiring Now - List. AngelList looked through their data to find which companies have added the most employees in 2019, and we selected the leading startups that also have open jobs. They removed any company that didn't include salary/equity data for its jobs. The list includes also companies like Roblox, BlackBird, Truly, and Looker. Prifina offers tools, including personal concierge and AI, and services to manage private data in the digital world. Prifina believes that people must be able to own their own data and have solutions to manage, control and utilize their data. Personal data is fundamental a part of personal wealth. Personal data is a part of personal life. Personal data influences personal life and personal data can have an eternal life. Prifina believes it should be in your personal control and your personal AI will serve you.  It has been a great privilege for Prifina to be invited to attend the largest family office meeting in Monaco. The Ritossa Family Office Investment Summit took place on June 18–20, 2019. A number of honorable members attended this event: His Highness Prince Albert II of Monaco, Sheik Abdulrhman Abuhaimin from Kingdom of Saudi Arabia, H.R.H. Prince Michel de Yougoslavie, and more than six hundred representatives of family offices, prominent conglomerate business owners, royal family members, private investment companies and industry professionals. Ritossa Family Summit is the largest gathering of family wealth in the world with $4+ trillion of wealth represented at the Summit. The organizers, Ritossa Family Office, is a family business dating back 600 years to the time of the Venetian Empire in Europe. During the two days of the Summit, Prifina team was fortunate to engage in numerous private conversations, network with industry leaders and technology visionaries. We were delighted to share our cross-border thought leadership about the future of data and management of private finances. Prifina’s team also participated in panel discussions about the practical aspects related to FinTech and offering financial services in the digital environment. Prifina’s CEO Markus Lampinen was also invited for an interview with CNBC where he explained the vision and of Prifina and how new data management tools are going to emerge in the forthcoming years. Here is the full interview: Robocorp has launched the first pilots of the Robocloud orchestration platform. The world's first cloud-native RPA orchestrator is designed to be a cost-effective, secure, fast, and scalable way to adopt and grow enterprise-level software robotics that has is built with open-source tools. Robocloud is a subscription-based cloud platform that enables secure deployment and orchestration of robotic process automation workers with minimum overhead. Robocloud’s technology allows creating a scalable RPA infrastructure for an organization within minutes. Robocloud has a flat monthly rate, which is significantly lower than any current competing solution on the market. The ten pilot partners are leading consulting and system integrator companies that especially focus on offering top-level solutions for robotic process automation. The partners plan to develop solutions, for example, to finance, transportation, and logistics companies. Partner feedback is used to guide product development and prepare for the 2020 public product launch. Robocorp is set out to change robotic process automation. RPA has the potential to change how millions of people work every day, and Robocorp is making it accessible to everyone through license-free open-source technologies and cloud delivery. More information Antti Karjalainen, CEO antti@robocorptech.com  Difitek Selected to Join the Leading Telco Carriers’ Launch of the Communications Blockchain Network6/25/2019 Difitek is delighted to support the Communications Blockchain Network (CBN) and its innovative solution that tackles settlements and aims at enabling modern services in the several billions dollar market of global ICT service providers. “We appreciate the opportunity to work with leading telco and blockchain companies in the specification and implementation stages, as well as in the operational stage. We will support the initiative offering our finance engine and open API framework that guarantees safe and compliant transactions, and an interoperable layer to interact with blockchains and other modern services.” Difitek’ CEO Armodio Corrado commented. See the full press release below. Atlanta, GA, Monday 24th June 2019 – The Global Leaders’ Forum launches Communications Blockchain Network (CBN)11 carriers invest in the set-up of a blockchain enabled settlement platform supported by over 10 technology partners The ITW Global Leaders’ Forum (“GLF”) today announced that it is launching a special purpose vehicle that will develop a live, blockchain-based platform, which will revolutionise the ICT Service Provider industry’s commercial settlement infrastructure, representing an opportunity worth billions to the global industry from costs savings and revenues from new products and services. The CBN, which is expected to go live in the coming months, will be governed by a collaborative structure. Several carriers have already agreed to support the establishment of the platform, with A1 Telekom Austria, China Telecom Global, Colt Technology Services, Deutsche Telekom Global Carrier, IDT, Orange, PCCW Global, Tata Communications, Telefonica, Telstra and TNZI all agreeing collaboration to ensure this blockchain-based, special purpose mechanism can become a reality. The GLF is also inviting every ICT Service Provider to join the CBN without any prerequisite. The GLF is also announcing that it will partner with leading technology providers to develop the reference architecture and support the creation of an open ecosystem for both ICT Service Providers and technology vendors. Over 10 technology providers have already confirmed their support for the platform and their intention to participate in its development, including Amartus, Clear Blockchain Technologies, ConsenSys, CSG and their Wholesale business, Difitek, IBM, Internet Mobile Communications, Orbs, R3, Subex, Syniverse, and TOMIA, with more to be announced. Blockchain, or distributed ledger technology (“DLT”), can provide significant benefits that will transform inter-service provider settlement processes by enabling automation and improving security. DLT-based automation can facilitate carriers to settle new types of traffic, underpinning network and service innovation, and save costs. The objective for the platform, and the collaborative industry-wide governance framework, is to serve the wider ICT community by avoiding fragmentation and thus help accelerate the adoption of automated settlement applications. The new environment will facilitate development of open-source standards and APIs that enable service-provider interoperability of DLT-enabled services, and manage critical infrastructure elements of the platform. Louisa Gregory, leading the GLF working group on blockchain and Chief of Staff of Colt, said: “For the past 14 months the GLF and its partners have been putting rigour and processes behind this platform and we believe that now is the time to launch. The blockchain-based ecosystem has been tested with resounding success at every stage, and we believe that this platform signals nothing less than the future of ICT financial settlement.” Marc Halbfinger, Chair of the GLF and Chief Executive Officer of PCCW Global, said: “When we set out along this journey, it was our goal to launch a platform that would enable multi-dimensional automation for the betterment of the industry. Now we are embarking on the next stage of this process by creating a truly open platform that will facilitate settlement among every ICT Service Provider, including carriers and cloud providers for all forms of ICT traffic.” Franz Bader, Director of Wholesale at A1 Telekom Austria said: “Making processes between carriers more efficient is only one of the huge potential benefits blockchain provides. Settlements will be our first step on that most promising path into the future. We are looking forward to many carriers joining us on that journey.” Rolf Nafziger, SVP of Deutsche Telekom Global Carrier, said: “Smart contracts and blockchain have a huge potential not only to simplify and automate complex inter-carrier billing/settlement processes but also to handle the complexity added by new services like NB-IoT, VoLTE, etc. To avoid fragmentation, it is very important that we move and work together as an industry. We therefore highly welcome and actively support the GLF initiative of an interoperable carrier blockchain network” Nick Ford, President of IDT’s Carrier Services, said “IDT is pleased to be part of the working group creating the GLF CBN. To focus on value for our customers, we all need to reduce the friction and costs of the back office. The CBN will be a platform to automate much of the basics between carrier partners, identify discrepancies before they become problems, and allow commercial, operations and finance teams to spend their time on elements of the business that make for differentiated service. We are happy to play a contributing role in pushing the industry towards blockchain settlement.” Emmanuel Rochas, CEO of Orange International Carriers, said “Orange has been involved from the start of the Blockchain initiative. The creation of this SPV to work along together with 11 other carriers is a significant advancement in business development and a new way of working towards the optimisation of telecom settlements processes.” Juan Carlos Bernal, CEO of International Wholesale Business for Telefonica, said “Blockchain will continue to deliver significant benefits across the entire wholesale sector. This important step forward showcases these real and tangible benefits from this technology and is also a positive reflection of the wider adoption of innovation in our sector.” Jussi Makela, Director of GLF said: “From very early on, the GLF recognised the importance of the right governance structure to provide certainty to the whole industry that the platform will be open, inclusive, independent and conducive of innovation. We are confident we have the right framework in place and we are excited to welcome every ICT Service Provider to participate in the development of the platform.” About the ITW Global Leaders’ Forum The ITW Global Leaders’ Forum (GLF) is a global network of leaders from the world’s largest International Carriers, who convene to discuss strategic issues and to agree collaborative activities, with the aim of upholding the principle of interoperability and ubiquitous international and technological coverage. The mission of the GLF is to be “the voice of the global carrier industry providing leadership and direction to interconnect the digital world”. This encapsulates the ultimate aim of the GLF, and its members, which is to enable consumers and enterprises to communicate and transact for any service or application, on any device and any infrastructure, in any geography, thus enabling the globalisation of business and the closure of the digital divide. The International Carrier industry is a critical part of the global ecosystem, providing the backbone that enables digital services to be distributed around the world. The GLF’s primary objective is to provide leadership and direction for the industry by advocating common priorities that will limit network fragmentation and improve interconnectivity so that new digital services can be delivered at scale anywhere in the world. More information is available at the company website: www.itwglf.com About Difitek Difitek provides the leading finance engine for digital finance services. It has powered many financial marketplaces in real estate in the US and Europe, in access to capital for individuals and small businesses in South East Asia and new forms of financing in South America. More information is available at the company website: www.difitek.com For further information, please contact: Armodio Corrado, CEO info@difitek.com +1 415 580 0087  Amazon started in the mid-90s. Online stores and e-commerce were also emerging in the 90s. We have talked about digitization for decades but only now do we start to witness a real purge of brick and mortar stores with many closing around the world. Why now, do changes really happen so slowly? But maybe the game is not yet over if retailers could just become innovators and change the rules of online commerce. Especially in the US and UK, thousands of stores have been closed or gone bankrupt during the last 12 months. Some other countries might be left behind and the big wave is only coming. In a way this has been expected for years, yet it is almost surprising, how long many traditional retail stores and chains have survived. They haven’t been able to change their business – they have just tried to delay the inevitable. Why is this happening now? We can assume some reasons:

The situation is a combination of many things, but it is very hard for traditional retailers to stop or delay the development. The only solution is that they must adapt to the situation. It requires them to become innovative. It is not enough that to simply open an online store when the big online players already have better resources and brand recognition to do it better. We can see some rising concepts that also offer opportunities for old retailers. For example:

As is expected in any battle, each party should focus on their own strengths and find the other party’s weaknesses. Customers are still looking for experiences, and physical stores and showrooms are a part of that, but they must be modified to support and improve customer experience and have clear ways to drive sales, offline or online. This requires a new type of concept and customer experience design that can definitely not be achived by cutting costs and product lines in existing stores. Data and privacy are another interesting area to change the game. Amazon and other leading online stores have accrued better customer data than traditional retailers. They can make better recommendations to customers and they can also better predict demand and manage their supply chain. Data helps them optimize their business and offer what customers want with better prices. Privacy is also becoming a more important issue and consumers are not so willing to give their data to those big players any more. We are also seeing that in the future consumers could own and control their own data. These kinds of distributed data models are the only option where smaller retailers could compete with leading online stores. Retailers could cooperate with parties that empower consumers to collect their own data and use their profiles to get better customer experience and the right products. This development will lead to personal AI that help consumers find what they really want. These new concepts are possible weapons for traditional retailers to fight against leading online companies. The concepts are not enough to win the battle or the war. It also requires superior execution. It also means these companies must renew their operations. They must become modern digital companies internally, with data-oriented processes. It means they must be ready to kill their old processes, operations and functions. To be clear, this doesn’t mean just using new software and IT for old processes, it means building new operations, processes and models from scratch. Many retailers are now in a death spiral. They still have many assets, but they could soon be gone, if they don’t build totally new businesses now. They must not only look at the 20-year history of online stores but find the new trends and areas where they can change the current online business and offer something better to customers. Customers look for good experiences, and price and data drives both business and consumers, too. Retailers really must become innovators in those areas. The article first appeared on Disruptive.Asia.  At least 1.5 billion adults worldwide do not have access to financial services. Those people are not benefiting from financial inclusion, or being part ofthe financial systems in any way. Despite this number having recently dropped, it is still a lot of people. Financial inclusion is also linked to human rights, opportunities to get a job, to have a home and access utilities. Those without financial services are not only in developing countries, but also in Western Europe and North America – but we can see hope that the situation is getting better. Opening a bank account depends on several factors. Banks want to choose their customers, and with tough KYC (know your customer) and AML (anti-money laundering) requirements banks are getting even more selective. Financial services now include many more options than just simple banking. Some obstacles people face to get access to financial services include:

The reality is that financial inclusion requires new models and a new way to conduct business. Technology, especially fintech solutions, can help a lot, but at the same time there is a requirement for business models that can include and encourage these new customers to come to and use the services. For example, in western countries it can include working with people and communities that are not just missing out on banking, but also other functions in society. Technology can help financial inclusion in many different ways. For example:

People can now start to use mobile wallets to receive salary and other payment, and international money transfers with at reasonable cost. They can also start to take small loans without credit history or permanent addresses, and in that way also build their finance history. At the same time, service providers can offer these services with lower costs and investments. Technology is really the key component for improving financial inclusion and equality. Financial inclusion is not only important for these people, but for the whole economy. When people are included in financial services, they can better work, use money, buy a house and save money. This is fundamental for all economies. It also means people can start to pay taxes. When many people are outside finance services, it is not only a problem for those people but for society and a country’s economy. Of course, this is not only about technology, but as we have seen many other areas, when a technology becomes commodity, it enables many new things. We see now this development in financial services. Many banks are still stuck with their legacy systems, but it doesn’t stop new players emerging that have newer, more cost-effective solutions. Beyond the technology, financial inclusion needs also the right attitude. It needs people who see opportunities to offer financial services to these excluded people. It is not altruistic thinking, it is also seeing opportunities outside the traditional ‘fat cat’ approach. One could also say, it is a choice, if you want to only handle the millions of dollars of a few people, or a few dollars from millions of people. With the traditional banking model, the latter option was not so attractive, but fintech has now made it a real choice and at the same time help these people, bottom lines and economies grow. The articles was first published on Disruptive.Asia. Difitek (a Grow VC Group company) offers platforms to build new finance services also for unbankable people, read more.  It is said that software consumed hardware and now data consumes software. Although software is core to most businesses today, it is not easy to create a viable software business, or at least generate big profits by only selling software. And to make matters worse, there is currently a global shortage of software people. What should we conclude from all this? Can companies make money from software? We see many trends in the software business:

When we look at these trends, it is plain to see that it is not easy to find a ready model to become a successful software company. One popular option is to sell top level software development capability, but that is not a very scalable model. Software companies must become more innovative, and we could even claim that business model competence has become more important in the software business than software competence itself – presuming you want to create something big. Microsoft used to be representative of traditional software business. It provided software licenses mainly for PCs. Hardware vendors paid forand supplied the MS-DOS/Windows operating systems but customers paid for Office, that has now become a cloud-based SaaS. Apple is a leading hardware and software company, but after people pay for their iPhones they use services like the App Store, for their apps, music and content. Google has until now offered its Android operating system for free, although it now plans to introduce license fees, yet its main target has been to gather user data, offer ads and provide content and apps through its Google Play platform. Then we have traditional B2B software companies like SAP, Oracle and Salesforce. Oracle has always had the most traditional license model. SAP also has license fees, but it is more a platform to develop actual applications. Salesforce, of course, is the famous SaaS pioneer, that now includes a lot of applications from third parties. Actually, all these cases give an indication on how software businesses are developing. In each case you need to offer a very scalable system; effective channels to get it to users; but also the opportunity to build niche and tailored services and apps on top of it. This is the platform economy model to offer software and it is important to get enough services, service providers and users to the platform. However, the quality of the services can be more important than quantity. It is hard to provide simple success factors for any software business (and even if I knew them, I probably wouldn’t publish them), but we can list components that seem to help:

Of course, many parties try to follow this route now. Quality and usability are probably the key success factor to be successful in this game. It is, for example, easy to make compromises on the quality and just focus on attracting lots of apps or developers, but this can be harmful in a longer run. Is data eating software? It is probably a topic for its own article, and it is not so simple. I think the comment is used to mean that it is more important to own and utilize data than software. It is clear that for companies like Google and Facebook it is like this, although they have good software to use data. Maybe Amazon belongs with these companies, too. But the latest issues with data misuse, breaches, and privacy make this more complex. Data will be important, but who owns it and who has the right to use it is becoming more complex. Maybe people will opt to get their own data back and be willing to use good software solutions to utilize it, like personal AI services. Business models are funny things. When a strategy consultant formulates a winning concept, innovative entrepreneurs work on the next big thing that will beat the old model. If you are a good software developer, you can make good money by coding, but if you want to create something much bigger, then you must innovate and create a new business model as well. The software business is like the music, movie or game business – you could make it big with some luck, but to build systematic success you need a platform and distribution channels to offer so much more than just luck. It is then more about orchestrating than coding. The article first appeared on Disruptive.Asia.  |

AboutEst. 2009 Grow VC Group is building truly global digital businesses. The focus is especially on digitization, data and fintech services. We have very hands-on approach to build businesses and we always want to make them global, scale-up and have the real entrepreneurial spirit. Download

Research Report 1/2018: Distributed Technologies - Changing Finance and the Internet Research Report 1/2017: Machines, Asia And Fintech: Rise of Globalization and Protectionism as a Consequence Fintech Hybrid Finance Whitepaper Fintech And Digital Finance Insight & Vision Whitepaper Learn More About Our Companies: Archives

January 2023

Categories |

RSS Feed

RSS Feed

|

Digital Intelligence Globally

|

© 2009-2023 Grow VC Operations Ltd. All Rights Reserved.

|