|

We have probably passed the peak of blockchain and cryptocurrency hype. It doesn’t, however, mean that nothing is happening with the technology and market at the moment. But it does raise the question, are we now approaching real blockchain business and more stable crypto solutions? And what is the status of public and private solutions? Can we really count on the security of blockchain-based systems? Can we have a generic blockchain or is it more to have application specific solutions? We are now hearing fewer fantasies about blockchain and crypto finance than a couple of years ago. This is a positive sign after the first peak of hype. At the same time, we can say that blockchain development hasn’t stopped. There are a lot of developments with the technology and a large number of pilot projects. Blockchain and crypto finance pilots include projects for supply chain, settlement, clearing, cryptocurrencies and voting models. There are also several projects including the tracking of coffee beans; smart contracts for beverage logistics; money transfers and international telco settlement. However, most of the pilots are quite limited, i.e. include a few parties that are committed to the pilot. The real target of blockchain is to be a multi-party system without an authority. Some blockchain activists also see that real blockchain must be always an open system, but some others see that private closed blockchains can still be relevant and valuable for many needs. But whichever approach we take, it is very important to get from low number party pilots to systems that include multiple parties. The next important target of blockchain pilots and PoCs (Proof-of-Concepts) is to get different companies and parties to work together with one system. It is technically an important step and really tests the capacity and technical compatibility of any solution. Just as important, if not more important, is that the blockchain and smart contract solutions should offer a non-authority, trustless system. There is not enough proof of a pilot’s viability if it only includes a few parties that know and trust each other. For example, JPMorgan has talked about its own cryptocurrency, but many parties see it purely as a digital currency, because it is a private system that only works between a lender and its clients. Many claim that it is hard, or even impossible, to have generic blockchain and smart contract solutions that can be used for all kinds of applications and contracts. It is felt that we need tailored solutions for different applications and business needs. Can we really expect blockchain solutions to take off with these limitations? Part of the complexity is that we have to create contract models with software, including special terms and conditions of the contracts in the software code. If we compare this to development of hardware and software solutions, one could claim that big breakthroughs happen only when it is possible to create layers for solutions, and properly isolate different layers and keep them generic. A clear layer model would also help with the security issues. If it is possible to use tested and better-known lower layers for contracts, then only the details and terms of the contracts would be case specific. There has also been quite a lot of discussion about the security of blockchain solutions. Especially for voting and identity systems where one realistic threat is plutocracy. Parties that have enough money and resources can basically buy votes. There seems to be several ways to do this depending on the implementation of the voting system, but it still appears to be hard to prevent this with the existing solutions. This is definitely one area, where new solutions are needed. A more acute threat now comes from 51% attacks – where a party can control enough (over half) of the computing capacity to mine a crypto coin and then basically create its own blocks. Only a few months ago this was seen mainly as a theoretical threat. A theoretical example touted was that some parties in China could coordinate such an attack in extreme situations. But now we have seen the first 51% attack on Ethereum Classic so it is no longer a theoretical threat! This has led to the development of more advanced versions of the proof-of-work algorithms. This is taking solutions more towards proof-of-stake algorithms. It is quite typical in all systems, including critical financial systems, to have vulnerabilities and updates for the software are constantly needed. But with blockchain this is more complex, when it is impossible or hard to undo transactions. The solution, for example to return stolen money, is to rewrite history and go back to the point before the attack occurred and recreate all ‘legal’ transactions after that so that all parties agree on those transactions and create new blocks. It is also a complex legal and ethical question, if the community has the rights to rewrite history. A strength and weakness of blockchain and smart contract solutions is that different parties can see and investigate the software core. It means different parties can also find potential bugs and vulnerabilities. If a party finds a problem, then it is up to this party, to determine how it wants to use the information, i.e. to either hack or improve the system. The blockchain hype also included theories that blockchain had no security issues and could solve all the issues of traditional financial systems. Of course, this is a naïve belief. All systems have their issues. The positive side is that many developers and parties are already active in the blockchain community constantly developing improved solutions. However, as with any system, it is a continuous race between threats, problems and better solutions. But blockchain is different from traditional centralized systems, and the risks and new solutions are different, and different competence is needed to handle them. Banks, stock exchanges, telcos, logistics companies and many startups are already working with blockchain solutions. Nothing, it seems, can stop this development path. As yet, we don’t know which blockchain solutions will make a real breakthrough and rule in the future. Maybe those solutions will be unlike existing blockchain solutions, or other distributed ledgers because computing and data are now distributed in many different ways. They must first solve the issues of existing solutions, especially getting from private pilots to multi-party transaction models. The article first appeared on Disruptive.Asia.  Grow VC Group and its portfolio companies participate in several events in May and June. They focus especially to present cases and new solutions for new finance and data models. This includes, for example, cloud based finance back office with open APIs, blockchain for several use cases and new solutions for consumers to manage their own data. The companies will be in the following events:

Grow VC Group is the global leader of fintech innovations, digital and distributed finance services, data services, and digital infrastructures. Our mission is to make the finance and data services more effective, transparent and democratic. Prifina gives you the power to collect, store and manage your data, in a secure and encrypted environment. Difitek provides a compliant, bank-grade secure and efficient technology framework for forward-thinking organizations of any size to launch and scale financial service. If you want to know more or come to meet Grow VC Group, Prifina and Difitek people in the events, please contact us.  Last year MWC was the time of minimum knowledge and maximum hype for blockchain. Now we have much less hype, but there are also much more real uses for blockchain. Edge has had much less general hype, rather it has been telco hype. But actually Edge and blockchain together can be components for true significant changes in internet services; to the point where the internet is not same anymore. For example, last year I was listening to a middle Asian telco describing a strategy to conduct bitcoin mining, because they have cheap electricity. I see great longer-term opportunities with blockchain and crypto finance, but listening to that made me feel bad. Fortunately, we have made a lot of progress during the last 12 months. This year MWC we had much more concrete and realistic cases for blockchain, for example, supply chain, settlements and data privacy. Several cases are still in the proof-of-concept phase, but this still reprents progress from vague ideas. Now the next very important phase is to get several parties in an industry and cross-industry to cooperate and really build working ecosystems. Blockchain related startup investments imrpoved to $3.9 billion last year from $1.1 billion in 2017, and estimated capital market spending in banking from $210 million to $315 million (source: McKinsey & Company). Accenture presented at MWC a blockchain case in supply chain. It includes, for example, ABInBev, Kuehne + Nagel and European Customs Authority to manage supply chain and logistics for beverage production. The PoC focuses especially on bill of lading process, when the whole logistics process still includes so many paper and EDI documents that it takes more time and effort to get all this on blockchain. Generally, blockchain is brought to services especially to bring traceability, immutability and decentralization. One case where all these components are important is tracking of coffee beans or other foodstuff items. It offers transparency also to consumers. Clear presented, together with Difitek, solutions to make settlement and clearing based on high performance blockchain solutions. Clear has especially worked to implement solutions to offer high capacity blockchain for solutions that require a lot of real-time or near real-time transaction processing. Difitek offers finance engine, back office and open APIs to integrated then these solutions to many finance systems and blockchains. Edge is, of course, totally different technology from blockchain, but the common attributions are distribution and de-centralization. Edge is now driven especially by telcos, because it is an opportunity for them to compete better with, for example cloud companies. In addition, Edge solutions must be near customers, where telcos are. But as with blockchain, to get to real success, it is important to get many different parties and industries to work together. If someone wants to be the central point of de-centralization, it is quite easy to see that something is wrong with that approach. Together Edge and blockchain can offer really exciting models for how data, computing, trust and verifications are distributed. Then we can see solutions where consumers manage their own data and AI, and basically carry their own data to interactions with vendors. Prifina is one company that develops this kind of solutions, and also testing blockchain and distributed storage solutions as components into the service. We are still living the early days of these de-centralized solutions. Regardless, it is clear that we are reaching an era where companies build real solutions based on real use cases, and pilot them with real users. The next phase is then to get many more parties to work together with these models. These solutions are built to connect many different stakeholders. Amazon, Facebook and Google are the giants of the centralized internet and data. Then we have banks and credit card companies that authorize most finance transactions. They won’t lose those positions quickly. But with the de-centralized internet, data and finance will have its own pioneers that change the world. Telcos can have a new role in this new era, as well as those established companies and startups that are ready to commit to build these new solutions now. The article first appeared on Telecom Asia.  MWC is an event to launch new products and solutions. At the same time, it is not really a place for disruptive innovation. It is more a place for the industry players to update their evolution. There are also startups, but not the kind that aim to truly disrupt anything. So, what is the innovation update for MWC 2019? And how will the good old digitization provide for something new? 5G, IoT, AI, and Edge are probably the most used abbreviations in this year. All those areas are making clear technological progress and there are new products available. But it is hard to see anything that would really be innovative and a game changer. Maybe foldable phones are something new, but actually rumors and pictures about a foldable iPhone looked more innovative (at least cooler) than anything at MWC. 4YFN is again dedicated for startups and future solutions. There are probably some companies that can make something significant in the future. But most startups are in those booths that are subsidized by different governments and they don’t really represent new innovation. There are companies that offer some data analytics for marketing, some technology components for networks and healthtech and all kinds of business application platforms. They might have nice technology and grow their business, but most of them don’t disrupt anything. With innovation we have also a question, if it is new technology or is it a truly new and valuable offering to customers. MWC has many things that can represent new technology but much less fundamental innovations that are already smooth consumer services. But on the other hand, there are things that are not very innovative technically anymore, but are now mature enough to offer value to users. Digitization is a strange topic. Some people seem to think it is something corporates must finally start with. Some other people say that it is the transition that is now on-going in most of companies. And then there are people who say we should not talk about digitization anymore, when it has been reality everywhere for years. What is even stranger is that all those people might be right. We have a lot of information in digital formats and data processing is a core of many activities nowadays. But it doesn’t mean that all activities are already digital and there are still many surprisingly old fashioned activities in most industries, including banking, telcos, logistics and retail. In some cases processes might be already digital, but they are not really designed for digital business. They are the old processes that just utilize computers and data. The difference between real digital companies and companies utilizing digital is huge. This might sound like a cliché, but just think about Amazon versus a smaller local retailer and their processes and use of digital technology. Industry 4.0 (including all other name variations in different countries) is one of those things that is very much linked to digitalization and also getting different industries to work together. The classical example, how production, logistics, retail and finance transactions must work smoothly together is still a good example, how cross-industry digitization and processes should work. Citi’s Global Head of Treasure and Trade Naveed Sultal emphasized at MWC especially the customer experience, and how it must be the starting point of digital services, including industry 4.0 solutions. He pinpoints the problem of many digitization projects. When traditional companies try to change the old processes to use computers and data, new challengers can build the whole company and customer experience based on the latest technology. Mr. Sultan also highlighted that “digital disruption poses an existential threat to some companies.” I would say it is like that for many companies. This can sound strange, when some people think digitization has been reality for years. But you can just look at how many retailers in the last and this year have been in trouble and even in bankruptcy in the US and UK, and many of them blame Amazon and online shopping. Things often take longer than we think and the big impact on industries comes with a delay. Retail and publishing businesses are seeing it now, but e.g. for finance it is still in a very early phase. MWC doesn’t typically have things that are game changers. But it is a place where many parties introduce and agree on small steps that are changing industries. It is an industry event, but one area many companies there should study more is how to become really customer oriented. Technology is an important enabler, but companies must really design their digital future based on the customer offering and experience. It is the real intelligent connectivity as this year slogan states. The article was first published on Telecom Asia.  San Francisco, March 11, 2019 – Difitek is pleased to announce the appointment of Armodio Corrado to the role of Chief Executive Officer (CEO) of the company, effective immediately. Former CEO Markus Lampinen who will continue to serve in his role as Board Director and Senior Advisor, will be taking on a new operating role within the Grow VC Group. Mr. Corrado has worked at Difitek since 2014 and previously served in the capacity of Chief Operating Officer (COO), before which he has worked with international finance and private equity. Mr. Corrado commented “I’m very committed about being in a position to steer the company to its next phase, where we are strongly positioned with our finance engine platform, and can support a wide range of clients and their success as digital finance gains maturity and wider adoption worldwide.” Markus Lampinen, Director and Senior Advisor commented: “Armodio has been a key pillar in the company for years and he is the right person to lead the company forward, empowering more clients with their digital products and focusing on delivering more customer oriented finance solutions around the world.” Jouko Ahvenainen, Chairman of Difitek Board comments the changes: " Markus has done amazing work to build Difitek from scratch to a significant company in the global fintech business. The company is now moving to a new era where it focuses on offering established technology solutions for all kinds of finance institutions and disrupting the whole finance IT market. Armodio has an excellent track record and foundation to continue this work to build the global operations and processes to serve customers. At the same time, I'm very pleased, Markus is moving to build a new significant business inside the same group to fundamentally disrupt the data business." About Difitek: Difitek provides the leading finance engine for digital finance services. It has powered many financial marketplaces in real estate in the US and Europe, in access to capital for individuals and small businesses in South East Asia and new forms of financing in South America. More information is available at the company website: www.difitek.com For further information, please contact: Armodio Corrado, CEO info@difitek.com +1 415 580 0087  Photo: Difitek CEO Armodio Corrado.

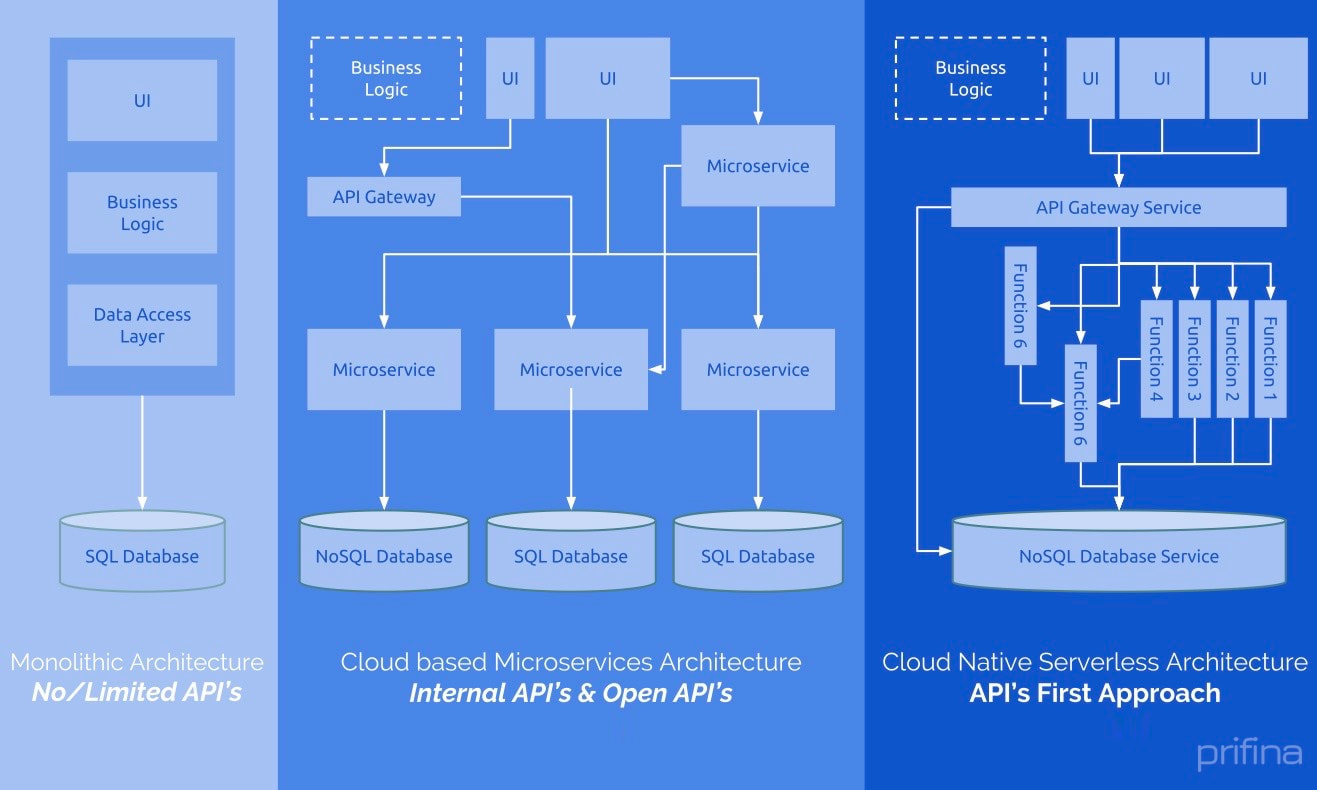

Simplicity was one important theme at MWC 2019. It is, of course, not a solution as such, but it a success factor for all solutions. This is nothing new, but it is becoming very relevant with 5G, IoT, data and security. Many parties can build technology, but who can offer simplicity to users will win. IoT enables the collection of data everywhere and control of devices everywhere. It will create billions or trillions of data and control points. But it is a very long way from all these sensors and devices to smart homes, smart cities and applications to help peoples every day life. 5G enables fast data connections to all those devices, creates local networks and communications everywhere and get many solutions to talk to one other. How users can really use them in an optimal way, use networks whenever wherever needed, but also manage privacy, use one way at home, another way when traveling or in the office. New opportunities will come from more versatile ways to manage the use of networks. Data and privacy have become real issues and discussion topics. Still many experts say people don’t care too much, they are ready to share data on Facebook, loyalty programs and online shops, and they are too lazy to be active to protect their data and take control of it. But the question really becomes what is the simplest solution. If data control and better security becomes as easy as buying from Amazon, posting on Facebook or showing your loyalty card, then we can expect people to take data control back. Technology companies haven’t always been good at thinking about simplicity. Of course, Apple is the famous example in terms of how they were able to bring simplicity to devices. Simplicity really doesn’t mean simple technology, almost the opposite. How to make really advanced technology that makes it easy to use services. It is especially about the user experience. Telcos are rarely leaders in simplicity. I still feel my mobile carrier’s app is one of the most complex apps I have, and hard even to check my monthly bill. Internet companies have been able to become successful in mobile too by offering simplicity and great user experiences. When mobile internet really started to arrive with 3G, then carriers talked a lot about walled garden models with their mobile portals. It was a kind of simplicity model. It was a nice model for carriers, but it was not really conceived from the user’s point of view. Now we hear comments about how 5G, IoT and Edge can give control for carriers in services. Yes, they can, but most probably they won’t give control until carriers are able and willing to give control to users and design services so that they are easy to use and simple for normal users. Commercial product management and UX are areas that would need much more focus, when we think the future of mobile and digital services. Now 5G and IoT presentations are often full of boxes representing tech nodes and lines between them. This technology view is needed, but it is not alone the solution, not even the starting point to design new services. A growing business area that offers a lot of opportunities is to offer solutions and platforms that make it easy for other companies to build new services and put less effort on building the technology from scratch. Vimeo is an example of this, their CEO spoke at MWC, and told how their goal is to make it easy for any company to make video communications and marketing. She summarized it as “any company can be like Netflix,” having no need to build its own technology, but focusing instead on their actual business. Similar solutions are emerging to develop, for example, digital finance and gaming services; finance and gaming engines and back offices. We will most probably see more solutions and platforms to build actual services and applications utilizing IoT, 5G and personal data too. Those services must also focus on how to simplify the actual services. It is positive to see simplicity is now an important theme at the event, but it is not yet the main theme. Most probably we still have a long way to go to see it in practice in all services. It is, anyway, quite sure, the winners of future 5G, IoT, data and security services are those who offer simplicity, not those who offer the most complex and messy diagrams. The article first appeared on Telecom Asia.  “M-Pesa is a great example of how money goes to the mobile, and telcos have a great opportunity to be banks in the emerging economies.” “Telcos are going to challenge banks in the emerging markets when services go to the mobile.” I have heard these sentences many times during the last 10 years. I would like to see something new and more concrete examples of telco forays into financial services. Is it just a nice dream? Or how will it become reality? M-Pesa started in Kenya in 2007. It has been successful there and expanded to offer more services like Google Play support and overdraft facility. It has expanded to other countries too, including Tanzania, Lesotho and India, where it has seen success too. Vodafone has executed it also together with local banks. But the expansion hasn’t been easy and in many countries the service has struggled and closed. M-Pesa was an excellent new service 10 years ago. But it alone doesn’t prove anything anymore about telco success in mobile money and payment services. Generally, there are not so many true success stories in this area. Several carriers have launched some mobile money or payment solutions, but we cannot say that telcos have got any significant role in this market. Ericsson and Nokia have also tried to offer platform solutions for this market. Nokia exited the market years ago, Ericsson has some clients for its mobile wallet. At the same time, new payment, lending and other finance solutions are really emerging in emerging economies. For example, in Indonesia, Vietnam and the Philippines dozens of millions of people are outside finance and banking services. This is a huge opportunity for new mobile and digital finance solutions. But is it realistic to think telcos could compete let alone this market? Telcos have played an important role in many services until mobile internet and mobile apps really came to dominate the market. Telcos encounter the same challenge if they want to enter the financial services segment. Many other parties already offer mobile apps for payments, banking, lending or money transfer. Feature phone market has been more secured to telcos (with M-Pesa originally especially an SMS based service), but there are also other platform vendors. You don’t need telco infrastructure to offer these services. Payment services are still the easy part. Real banking services, lending and investing services are much more difficult to execute. They are heavily regulated, require capital and put also capital to risk. Telcos are not really willing or able to take these kinds of risks. There have been a lot of discussions over if Apple or Amazon would start banking services. They have huge balance sheets and they could link them to support their other businesses, but even they seem to hesitate. Technically it is quite straightforward to implement digital finance services. There are platforms that offer the infrastructure and regulated services, like TagPay for feature phone payments, Difitek for digital and mobile banking, lending and investing services, and several mobile payment solutions from bar code models to blockchain. This means that technology is not really the bottleneck, but the mobile service company must fulfil the regulatory requirements and be able to operate finance business, including risk management. It is a good question - if finance services are really relevant for telcos to offer. It might be that they are not really for them. But why there are still all these stories and speculations, how telcos could come to the finance business. Maybe it is lack of information, dreaming or too technology oriented thinking. Probably the most feasible model for telcos to enter the finance business is with good partners that can offer the right technology, take the finance risks and offer the needed capital. Telcos have some interesting projects like the blockchain based settlement that could be expanded one day to global money transfers too. Telcos are not able to become real finance service providers, but they can be in an important role as part of consortia offering future digital and mobile finance services. The article originally appeared on Telecom Asia.  Serverless cloud services are coming and they will change the way we build software and design services. At the same time, they offer totally new business opportunities, especially for growth companies. Scalability is something very real with serverless, but it is not the only interesting aspect. AWS Lambda, Google Cloud Functions and Microsoft Azure Functions already offer serverless infrastructure, but most companies are still in a very early phase to really utilize it. One factor is the lack of competent and experienced developers. Grow VC Group already offers a trainee program for developers. At the same time, companies haven’t yet been able to properly consider, how to really get business value from serverless solutions. Serverless means dynamic allocation of server resources, i.e. no need to pay for dedicated servers, but being able to buy computing capacity, and use it, based on actual needs. Serverless models also change software architecture. The microservices model means that each small task or job is a separate function that works independently. This concept makes it easier to implement API services that can execute a process in the background and an API call doesn’t lock any other services. Serverless solutions can also offer better security against some threats. For example, a serverless solution is more immune to distributed denial of service (DDoS) attacks.  Those are technical benefits, but at the same time, this offers opportunities for new business models. Let’s consider that they:

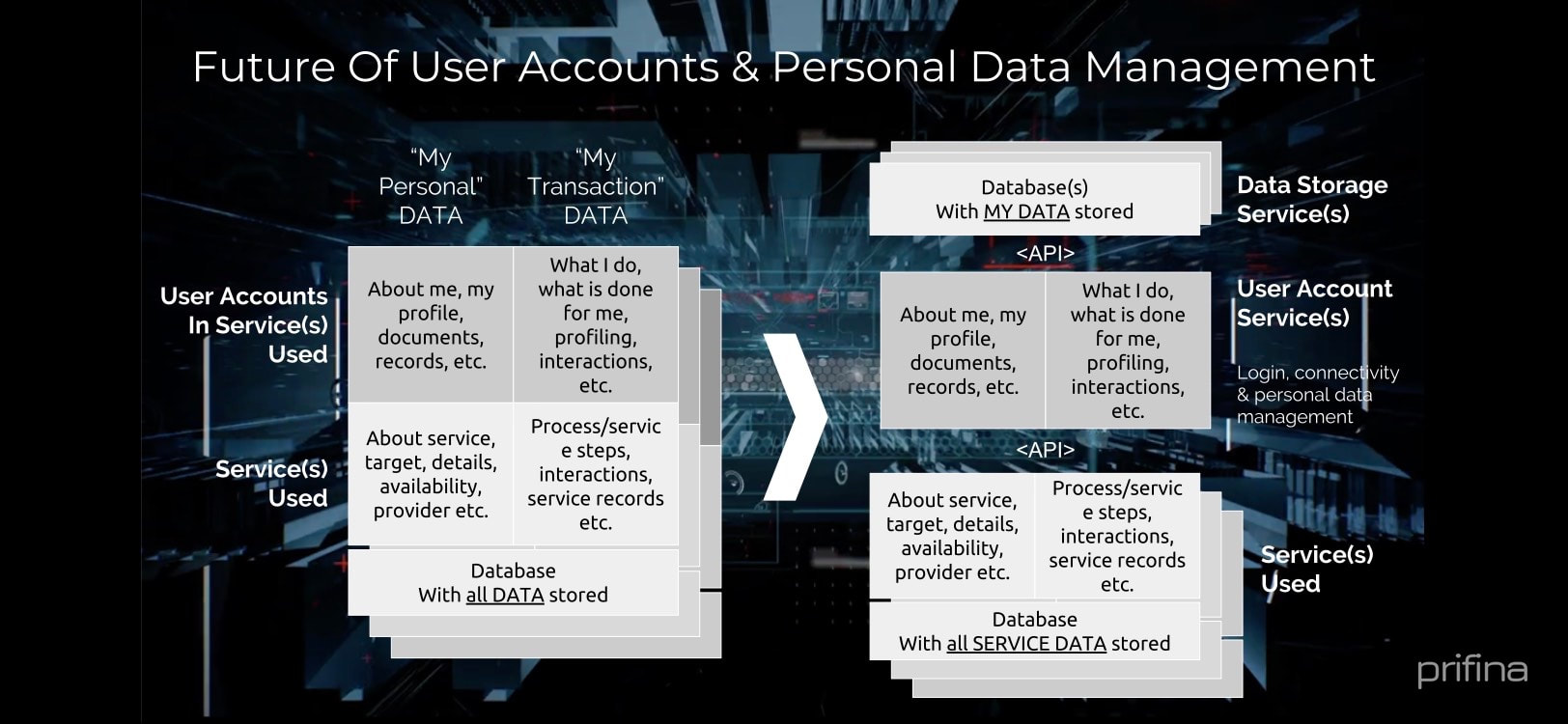

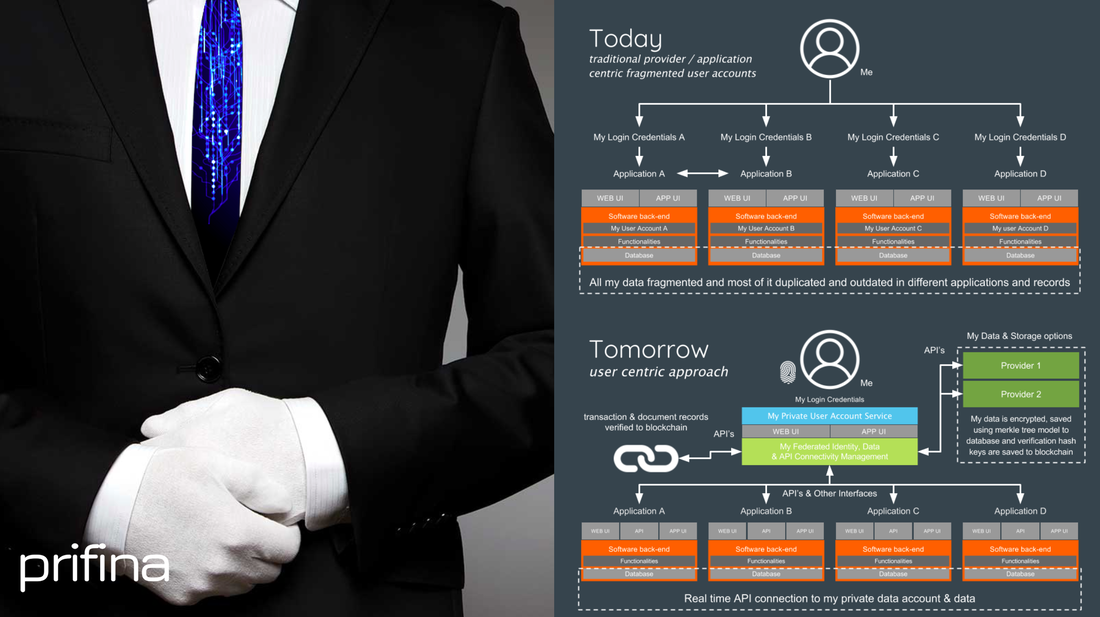

Micro-functions will probably be the basis for many new opportunities. By offering ready-made micro-functions to other parties and users, they will also become a component to distribute computing and data to many places globally. This is great, for example, for IoT, blockchain and latency critical services. There is currently a lot of planning and development going into making more distributed services, for example: local AI with local data; smart contracts without central authority; or Edge computing. Some data and computing can be undertaken in user devices, but it is not really the solution for all needs, if solutions need more data, they must be connected all the time or require really high reliability. Then one natural solution is to have more locally distributed cloud services. Amazon Lambda Layers now offers new opportunities to share common components and code. This includes the opportunity to build services that have a lot of users and can have flexible user-specific and shared components. It enables more local and customer-specific services, but it can open new opportunities for new AI solutions and the development new distributed AI algorithms. Serverless has also its own issues. It is still in early phase, and it needs more competent developers, better tools to monitor and debug services and better understanding and models to manage data and security aspects. But especially it needs companies to start utilizing its opportunities and offer real value for serverless service users. Serverless is a much less hyped new solution than AI, blockchain or Edge. Of course, the full potential of AI will be much larger, but AI is still a very unclear area (at least, how the AI term is used), whereas serverless is very concrete and available now. Many companies have looked at it only from a technical point of view, or how much they can save on server costs. They have ignored that the new model also offers new business opportunities. 2019 will bring much more serverless services and much more companies will start to utilize the technology. It is still hard to say, when business people and startups start to really explore its new business opportunities. It can be the crucial next step to more distributed computing, service and data models. The article first appeared on Disruptive.Asia.  Grow VC Group and other shareholders sold Kapipal to another crowdfunding service. Kapipal website and all active campaigns have temporarily been closed. The new owner will decide how Kapipal will be re-opened in the near future. You can follow news at kapipal.com. Grow VC Group started to work with crowfunding services in 2009 and was the pioneer especially in the equity crowdfunding. We have participated to develop finance regulation in many countries. In 2012 we decided to focus on more significant growth businesses in fintech, including technology platforms, data and digitization in finance services. Kapipal was the last crowdfunding business in our portfolio. We see great growth in many areas of fintech, finance data and digital platforms, and continue our work in those areas. Our companies offer, for example, a one-stop-shop to operate digital finance services, solutions people can own and manage their personal finance data, and Robotic Process Automation. Kapipal and its former shareholders would like to thank everyone who crowdfunded on the platform and were able to raise money for their dreams. Crowdfunding will help people, startups and innovators also in the future, and Grow VC Group continues to disruption finance sector in many areas.  Equifax, HSBC, British Airways, Cathay Pacific, Marriott, Quara – and we could continue the list much further. They are some of the companies that have had a significant customer data breaches this year or last. Does anyone believe their data is really safe with any company? Should we have totally new models to protect and use data? These cases have demonstrated that hackers can get to most companies and steal your data – if they really want to. Name, address, passport details, credit card numbers and passwords of hundreds of millions individuals have been stolen this year alone. After a breach, some companies have offered their credit score and identity theft protection services for free. I wrote earlier about the avocado model to consider for data protection, making a difference between hard core data and data that is less critical. It is one example of new paradigms to better focus on critical data and detect attacks. But many companies are still in a very early phase with their plans to change the paradigm. They still believe that just by putting bigger locks on the main door they are safe. It is also often said that the worst scenario is not that your data is stolen, but if someone is able to modify your data you could lose your credit score, be seen as a criminal or terrorist and be unable travel and get a visa anymore. This can happen, if criminals get access to data and don’t steal it, but simply modify it. We can also have many other terrible scenarios like nuclear weapons, airplanes, food processes and many other things, if the data is compromised. Distributed data Blockchain and distributed data models have gotten plenty of interest during the last two years. Cryptocurrencies and tokens have dominated the discussion but significant technological and data model concepts have received less attention. These also offer new models for data management and protection. Distributed data models are not necessarily based on blockchain or only on blockchain. The important part is that there is no one party that collects and keeps all data for a certain purpose. These solutions can offer several new offerings to better protect against stealing or misusing of data, for example:

These are changes that don’t happen rapidly and we have a lot of legacy systems and ‘experts’ to handle data management. It is, anyway, quite clear that problems and risks cannot be handled only with traditional models. Many companies now just try to buy time for their old ways to manage data. Consumers haven’t been too keen to worry about or protect their data. This year has been a turning point, but the reality is that people still look for easy solutions. We can expect changes only, when there are easy enough options for consumers and companies to protect and use their data in a new way. We already see startup activities in this area, and it is a matter of time, when we start to see more mainstream solutions. The article first appeared on Disruptive.Asia.  |

AboutEst. 2009 Grow VC Group is building truly global digital businesses. The focus is especially on digitization, data and fintech services. We have very hands-on approach to build businesses and we always want to make them global, scale-up and have the real entrepreneurial spirit. Download

Research Report 1/2018: Distributed Technologies - Changing Finance and the Internet Research Report 1/2017: Machines, Asia And Fintech: Rise of Globalization and Protectionism as a Consequence Fintech Hybrid Finance Whitepaper Fintech And Digital Finance Insight & Vision Whitepaper Learn More About Our Companies: Archives

January 2023

Categories |

RSS Feed

RSS Feed

|

Digital Intelligence Globally

|

© 2009-2023 Grow VC Operations Ltd. All Rights Reserved.

|